Buying a Car After Moving to Alberta from Another Province

In this article

- Alberta Is Booming — And You're Not Alone

- The Legal Checklist: What You Must Do After Moving to Alberta

- Alberta Driver's License — 90-Day Deadline

- Alberta Vehicle Registration

- Alberta Auto Insurance

- How Your Credit History Transfers to Alberta

- Establishing Alberta Credit Quickly

- Vehicle Needs Differ Depending on Where You Came From

- If You're Coming from BC

- If You're Coming from Ontario

- If You're Coming from Quebec

- If You're Coming from Saskatchewan or Manitoba

- What the Alberta Auto Market Looks Like for Out-of-Province Buyers

- Why Airdrie Makes Sense for New Albertans

- What to Bring When You Apply for Financing as a New Albertan

- Common Mistakes New Albertans Make When Car Shopping

- Understanding the Alberta Financing Landscape

- Your Next Step

- Related Buyer Guides

- Compare and Apply

Check Your Options in 3 Minutes

No credit impact. All credit situations welcome.

★★★★★ 96+ Google Reviews · AMVIC Licensed · Free Delivery 300km

You just landed in Alberta — new job, new address, maybe a new chapter entirely. Whether you moved for work in the energy sector, chased lower taxes, or followed family, one thing becomes clear almost immediately: you need a vehicle, and you need one fast. Alberta's cities are spread out, transit is limited outside of Calgary's core, and winters here are serious enough that whatever you're driving from your old province may not be properly equipped. The question isn't whether you need a car — it's how to get into the right one as quickly and affordably as possible when your Alberta life is still brand new.

See what you pre-qualify for

Three quick answers — soft check, no commitment.

Alberta Is Booming — And You're Not Alone

Alberta has been one of Canada's fastest-growing provinces for three consecutive years. The combination of no provincial income tax, a thriving resource economy, and relatively lower housing costs compared to Vancouver or Toronto has drawn hundreds of thousands of people from BC, Ontario, Quebec, and beyond. Airdrie alone has grown from roughly 65,000 residents to over 80,000 in just a few years, placing it among the fastest-growing cities in Canada. Calgary's population crossed 1.4 million in 2024, and the metro area continues to expand rapidly.

That wave of newcomers creates a common set of challenges at the dealership level. Lenders and dealers across Alberta see this situation constantly: someone with a solid credit history from another province, a legitimate new job, but zero Alberta track record. The good news is that this is a well-understood situation with real solutions. You are not an edge case — you are the most common type of customer we see walking through the door in a given month.

The even better news: your credit history moves with you. Canada uses a national credit reporting system through Equifax and TransUnion, so a strong score built in Ontario or BC is just as valid in Alberta. You are not starting from zero — you are starting from wherever you left off, with the added wrinkle of a new employment and address history that needs to be explained clearly to lenders.

The Legal Checklist: What You Must Do After Moving to Alberta

Before you shop for a vehicle, understand your administrative obligations. Alberta has specific timelines that affect both your ability to drive legally and your ability to finance a car. Missing these deadlines creates complications that are entirely avoidable.

Alberta Driver's License — 90-Day Deadline

Once you establish residency in Alberta, you have 90 days to exchange your out-of-province driver's license for an Alberta one. This is not optional — driving on an expired timeline with an out-of-province license creates insurance complications and can void coverage in the event of an accident. The exchange happens at any Alberta Registry office and is typically straightforward for other Canadian provinces. Bring your current license, proof of Alberta address (a lease agreement or utility bill), and government-issued identification.

If you arrived from BC, Ontario, or Quebec, the exchange is reciprocal and you won't need to retest for most license classes. Some American states require a knowledge test or road test. Check Alberta.ca for your specific province or state before going in, and book an appointment at your local registry to avoid long walk-in waits.

One practical note: when you apply for a car loan in Alberta, lenders will ask for ID. Your out-of-province license is valid for the 90-day window, but having your Alberta license in hand speeds up documentation — especially if your previous address on the old license doesn't match your new Alberta address on the application.

Alberta Vehicle Registration

You have 90 days to register your vehicle in Alberta after establishing residency. If you're buying a new-to-you vehicle in Alberta, it will be registered provincially at the time of purchase — the dealership handles this as part of the transaction. If you're bringing a vehicle from another province, you'll need to complete the out-of-province registration process, which includes an Alberta-certified inspection, new Alberta plates, and updated registration documents.

For out-of-province registration, budget for the registry fee (roughly $84-$100 for a two-year passenger plate), the out-of-province vehicle inspection if required (not all out-of-province vehicles need one, but it depends on age, province of origin, and vehicle history), and applicable taxes. The 2026 Alberta vehicle registration fee breakdown covers exact amounts by vehicle type and registration period so you know what to expect before you walk into the registry.

Alberta Auto Insurance

Alberta has its own insurance framework administered provincially, and rates are determined by your driving record, the vehicle you're insuring, your postal code, and your claims history — all of which transfer from your previous province. Contact your existing insurer first: many national carriers including Intact, Aviva, and TD Insurance operate in Alberta and can transfer your policy with a relatively simple process.

If you need to switch insurers, get quotes before purchasing a vehicle. Insurance rates vary significantly by vehicle type in Alberta, and some models that were inexpensive to insure in BC or Ontario carry higher premiums here due to regional claims frequency. An article on how your vehicle choice affects Alberta insurance costs is worth reading before you commit to a specific model — choosing a less popular theft target or a model with lower regional repair costs can save you $50-$100 per month in premiums.

One Alberta-specific note: Alberta is a direct compensation province for auto insurance. If you're in an accident that's not your fault, you deal with your own insurer rather than the at-fault driver's. Understanding this before you need to use it is useful context.

How Your Credit History Transfers to Alberta

This is the question newcomers ask most often, and the answer is reassuring. Equifax and TransUnion are national bureaus. Your credit file follows you — every credit card, loan, mortgage payment, and account from your previous province appears on your Alberta credit pull. A strong score built over years in Toronto or Vancouver is fully recognized here. You don't need to rebuild from scratch just because you crossed a provincial border.

What lenders in Alberta care about beyond the raw score:

- Employment history: If you're in the first 90 days of a new Alberta job, some lenders want to see your employment letter and first pay stub. Others are flexible with a firm offer letter. Probationary employment is workable — just be upfront about it in your application and bring documentation.

- Residence stability: Most lenders look for a consistent address history. If you're in a short-term rental or temporary housing after the move, bring a lease agreement or current utility bill showing your Alberta address. Even a month at the new address is enough to document.

- Debt-to-income ratio: If you're still carrying a mortgage on a property in your old province while renting in Alberta, lenders will factor that debt load into their calculations. Be prepared to explain the situation clearly — and if the property is sold or being sold, have documentation ready.

- Credit score tier: Prime borrowers (660+) have the widest lender pool available. Near-prime (600-659) and subprime (500-599) borrowers have fewer options but still meaningful ones, especially through specialty lenders who understand the newcomer-to-province profile.

If you're financing for the first time in Alberta through a subprime or near-prime lender, the newcomer car financing page explains exactly what documentation to bring and how lenders assess your file as a recent arrival. Being prepared with the right paperwork is often the difference between a same-day approval and a week of back-and-forth.

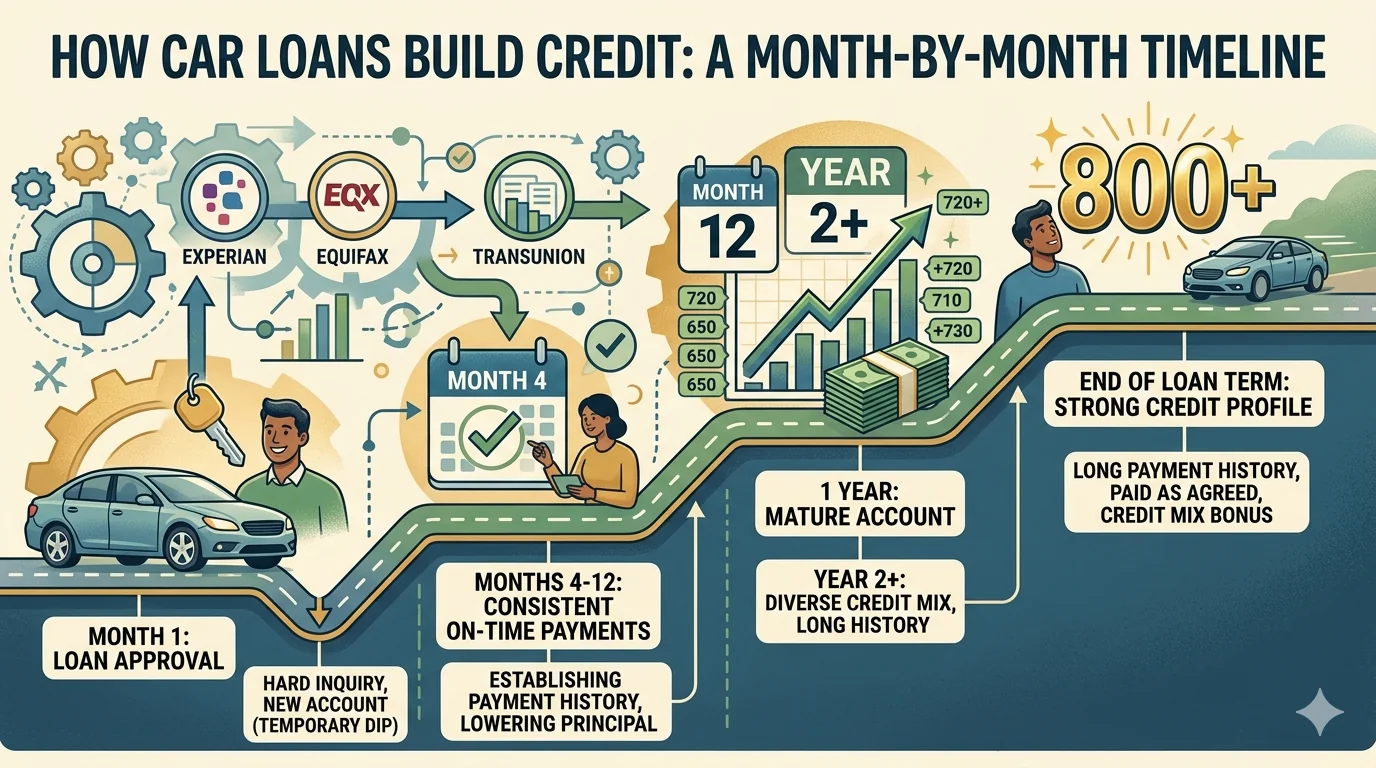

Establishing Alberta Credit Quickly

Even with a strong national credit score, having Alberta-specific credit activity can speed up approvals and improve your terms over time. Lenders look for local stability signals — and there are practical ways to generate them quickly without taking on unnecessary debt.

- Open a Canadian bank account with an Alberta branch address. If you haven't already, this establishes a local banking relationship immediately. The account statement becomes one of your strongest proofs of Alberta address.

- Get an Alberta utility in your name. Electricity (ENMAX or ATCO depending on your area), natural gas, or internet accounts become both address verification and, for some bureaus, positive payment history when reported.

- Apply for a credit card through your existing bank. Activating an account tied to your new Alberta address creates a fresh tradeline with a local association. A low-limit card used responsibly and paid monthly costs nothing in interest and builds credit history quickly.

- Finance a vehicle through an Alberta lender. The car loan itself is one of the most powerful credit-building tools available. Monthly installment loans are among the highest-impact tradelines on a credit file. A well-managed auto loan in your first Alberta year does more for your local credit profile than almost anything else.

For first-time car buyers in Alberta — including those who financed vehicles in another province but never in Alberta — the process is similar to a new credit applicant. Strong national history plus an Alberta address plus employment documentation typically gets you into a loan. The terms in year one may not be perfect, but 24-36 months of clean payment history opens significantly better options for your next vehicle.

Vehicle Needs Differ Depending on Where You Came From

This is something out-of-province buyers often don't anticipate. The vehicle that served you perfectly in Metro Vancouver or the GTA may be significantly under-equipped for Alberta conditions — or may need specific modifications before its first Alberta winter. Understanding this early saves money and prevents unpleasant surprises in January.

If You're Coming from BC

British Columbia mandates winter tires on many mountain highways from October 1 to April 30, so Interior BC drivers are often well-equipped for Alberta winters. But coastal BC — Metro Vancouver, Victoria, the Sunshine Coast — has mild, wet winters that don't require the same cold-weather preparation that Alberta demands. Vehicles from the Lower Mainland frequently lack block heaters and have batteries optimized for mild temperatures rather than extreme cold starts.

True cold-weather preparedness in Alberta means:

- Winter tires rated for temperatures below -30°C. Look for the mountain snowflake symbol (three-peak mountain with snowflake), not just the M+S (mud and snow) rating. M+S tires lose significant grip below -7°C. Alberta routinely hits -25°C to -40°C in January and February.

- A block heater. Almost every vehicle sold or registered in Alberta has one, but BC vehicles often don't — especially those from the coast. A block heater guide explains what it does (keeps engine oil from thickening overnight so your engine starts smoothly), why it matters (extends engine life significantly in cold climates), and what installation costs ($150-$300 at most shops).

- Synthetic oil rated for cold starts. 5W-30 or 0W-20 depending on your engine. Conventional oil thickens in extreme cold and creates momentary oil starvation at startup — where most engine wear actually occurs.

- A battery tested for cold-cranking amps. Coastal BC's mild winters don't stress batteries the way an Alberta January does. A battery that's three or four years old and was tested in mild conditions may fail its first real Alberta cold snap. Have it tested at any Canadian Tire or battery shop before winter.

If You're Coming from Ontario

Ontario drivers are generally better prepared for cold — Toronto winters are real, and much of rural Ontario gets serious cold and significant snowfall. But Alberta cold is drier, often more extreme, and the chinook cycle (rapid warming to +10°C followed by a return to -30°C within 48 hours) is hard on vehicles in a way that a steady Ontario winter isn't. Temperature swings like that stress door seals, rubber gaskets, and fluids in ways that don't happen in stable cold climates.

Block heaters are standard in Alberta vehicles and widely used. If your Ontario vehicle doesn't have one, budget $150-$300 for installation. Your four-season or all-season tires may meet Alberta's minimum road requirements on most highways, but dedicated winter tires are strongly recommended for the QE2 corridor in winter and are essentially mandatory if you're going into the Rockies.

See the winter car care guide for Alberta for a full seasonal checklist — it covers everything from battery maintenance to block heater best practices to what to keep in your trunk during a cold-weather emergency.

If You're Coming from Quebec

Quebec mandates winter tires from December 1 to March 15, so you already know winter driving. Your vehicle habits translate well to Alberta, and the gear you have is likely appropriate. One thing to verify: Alberta doesn't have province-wide annual emissions testing the way Quebec's Contrôle Technique does. Some Alberta municipalities have local air shed requirements — check with your local registry on arrival.

If You're Coming from Saskatchewan or Manitoba

Prairie drivers adapt fastest to Alberta conditions because the climate is similar. If you're coming from Saskatoon or Winnipeg, your vehicle is already equipped for cold. The main difference is terrain — Alberta's foothills and mountain approaches require AWD or 4WD if you plan to drive west of Calgary regularly. A two-wheel-drive prairie vehicle handles Calgary and Airdrie just fine in normal conditions, but the roads to Banff and Canmore are different.

What the Alberta Auto Market Looks Like for Out-of-Province Buyers

Alberta's used vehicle market has some characteristics that differ from other provinces. Demand is high, driven by ongoing population growth, and inventory quality tends to be good — Alberta's dry climate means less rust than Ontario or Atlantic Canada. However, hail damage is a real consideration. Alberta experiences more hail events per year than almost anywhere else in Canada, and vehicles with hail damage can have significantly suppressed trade-in values even when structurally sound. Always check a vehicle's Carfax or AutoCheck history for hail claims before purchasing.

Prices in Alberta have moderated from the pandemic peak but remain above pre-2020 levels. Your budget expectations from another province may need adjustment. A $20,000 budget that bought a 3-year-old compact SUV in Ontario in 2019 buys a 5-6 year old equivalent today. Building realistic expectations before you shop prevents frustration at the dealership.

Why Airdrie Makes Sense for New Albertans

If you're settling in the Calgary metro area, Airdrie deserves serious consideration as a base of operations. Compared to Calgary's inner-city neighbourhoods, Airdrie typically offers newer construction, lower property prices per square foot, and a tight-knit community feel that's genuinely different from a large-city suburb. The commute to Calgary via the QE2 is 20-35 minutes in normal conditions, and carpooling options exist for major employment corridors.

For vehicle shopping, Airdrie has the advantage of lower overhead costs for dealerships compared to Calgary's core, which can translate to more competitive pricing and a less high-pressure buying environment. Our team at Shift Happens operates in Airdrie specifically because the value proposition for buyers here is genuinely strong — you're not paying for a flashy showroom or prime commercial real estate in your vehicle price.

Calgary remains the commercial hub for the region, with the most inventory and the widest range of makes and models available on any given day. If your job or lifestyle is centered there, many of our clients commute from Airdrie daily on the QE2. The highway commute with a reliable vehicle is a trade-off most Airdrie residents find worthwhile given the cost-of-living difference.

What to Bring When You Apply for Financing as a New Albertan

The documentation list for out-of-province applicants is slightly longer than a typical Alberta resident's, but nothing difficult to gather if you're organized about it. Coming in prepared reduces approval time from days to hours in most cases.

- Valid ID (your out-of-province license is accepted during the 90-day exchange window)

- Proof of new Alberta address — lease agreement, recent utility bill, or bank statement dated within 60 days

- Employment letter and most recent pay stubs from your Alberta employer

- Previous two years of Notices of Assessment (NOAs) from the CRA if self-employed or if income varies significantly year to year

- Insurance binder or confirmation letter from your insurer showing Alberta coverage on the vehicle you're purchasing

- If bringing a vehicle for trade-in: original ownership documents from your previous province (these will be surrendered as part of the Alberta registration process)

- If carrying a mortgage on a property in your former province: most recent mortgage statement showing the balance and monthly obligation

With this package ready, most lenders can turn around a decision quickly. Our multi-lender model means your application goes to 15+ lenders simultaneously — so if one lender is more conservative on new-to-province files, another may be more flexible. You get the best available offer rather than a single institution's interpretation of your file.

Common Mistakes New Albertans Make When Car Shopping

After seeing hundreds of out-of-province buyers come through, a few patterns emerge that cost people time, money, or both.

Mistake #1: Waiting for permanent housing before buying. You need a vehicle immediately. Month-to-month rental addresses are accepted by lenders — you don't need to wait for a mortgage approval or a long-term lease to get financing started.

Mistake #2: Assuming their vehicle is winter-ready. Check your tires, your block heater, and your battery before your first Alberta November. Don't find out your battery isn't cold-weather rated at 7 AM on a -28°C morning.

Mistake #3: Applying to a single bank and stopping at no. A single bank saying no does not mean Alberta financing is unavailable to you. Subprime and near-prime lenders specialize in situational files, including newcomers in probationary employment. Our lender network exists specifically for these situations.

Mistake #4: Overbuying on the first Alberta vehicle. Your first Alberta vehicle might not be your vehicle for the next 10 years. Start with something reliable and affordable — upgrade in 2-3 years once your Alberta financial footprint is established and your credit tier has had time to reflect your new stability.

Mistake #5: Not getting a pre-purchase vehicle inspection on an Alberta used vehicle. Hail damage, in particular, is not always obvious on a walk-around. An independent mechanical inspection ($100-$150 at most shops) gives you full visibility before you sign anything.

Understanding the Alberta Financing Landscape

Alberta has a mature subprime lending ecosystem that has developed alongside its resource-economy boom-bust cycles. Lenders here are experienced with situational files — people who have strong income but irregular employment histories, newcomers with clean credit but no local track record, and workers who have had difficult financial periods tied to oil price downturns. This context works in your favour as an out-of-province buyer.

Our financing terms run from 12 to 96 months with biweekly payments standard across our lender network. Rates range from 6.99% for prime borrowers to 29.99% for deep subprime situations. A realistic example for a near-prime newcomer: a $22,000 vehicle financed over 72 months at 12.99% comes to approximately $198 biweekly. That's a payment most Alberta households can manage while getting established, and it builds the credit history that gets you into better terms on the next vehicle.

Your Next Step

Moving to Alberta is a big deal. Getting into the right vehicle quickly lets you get to work, get oriented, and get on with building your Alberta life. Whether you're dealing with fresh employment, no local credit history, or a trade-in from another province, options exist — and they're more accessible than you might think.

Use our approval quiz to check your likely range before walking into a dealership — the can I get approved tool takes two minutes and gives you a realistic picture of where you stand. When you're ready to move forward, the financing application takes about five minutes and goes to our full lender network simultaneously. Our team has helped hundreds of out-of-province newcomers get into reliable Alberta vehicles at payments that work for a new start — and we know exactly how to present a newcomer file to the lenders most likely to approve it.

Compare and Apply

- Complete Bad Credit Car Buying Guide (Alberta) — your complete Alberta subprime buyer guide

Financing Resources

Related Articles

Ready to Find Your Vehicle?

Browse our inventory or apply for financing. All credit situations welcome.

★★★★★ 96+ Google Reviews · AMVIC Licensed · Free Delivery 300km