How Car Loan Amortization Works: Where Your Payments Actually Go

In this article

- What Amortization Actually Means

- The Math: A Sample Amortization Table

- How Your Interest Rate Changes Everything

- Why Shorter Terms Save Dramatically More Than You'd Think

- How Extra Payments Change the Amortization Curve

- Biweekly vs. Monthly Payments: The Hidden Advantage

- How a Rate Drop Reshapes Your Entire Amortization Schedule

- The Amortization Math in Subprime Financing: What to Expect

- What Amortization Means for Your Equity Position

- Reading Your Loan Statement

- How to Use This Knowledge When Buying

- Related Buyer Guides

- Compare and Apply

Check Your Options in 3 Minutes

No credit impact. All credit situations welcome.

★★★★★ 96+ Google Reviews · AMVIC Licensed · Free Delivery 300km

Most people know roughly what their biweekly car payment is. Very few know how much of that payment is buying them actual ownership of the vehicle versus paying the lender for the privilege of using their money. If you've ever wondered why you still owe so much after two years of faithful payments, car loan amortization is your answer — and once you understand it, you'll never look at a loan term the same way again.

See what you pre-qualify for

Three quick answers — soft check, no commitment.

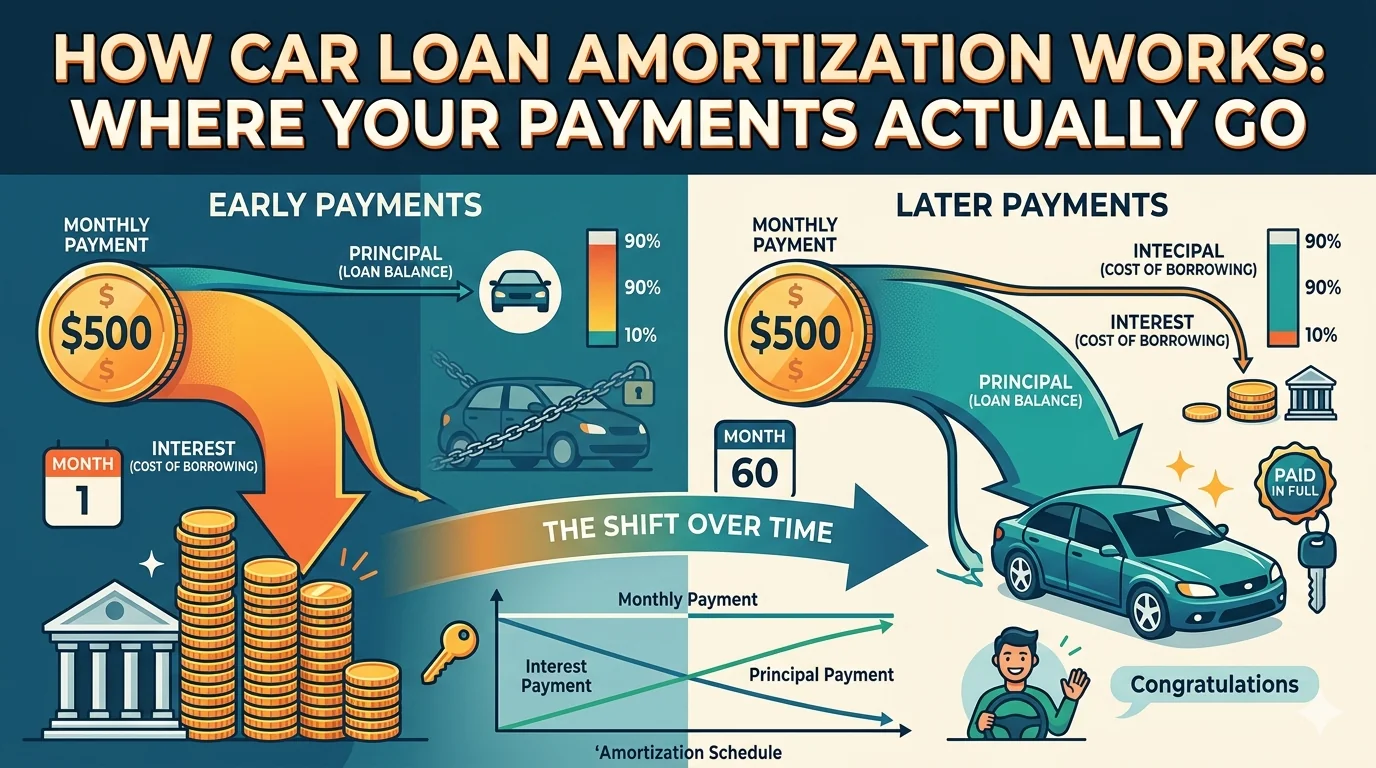

What Amortization Actually Means

Amortization is the process of paying off a loan through regular, scheduled payments over a fixed period. Each payment is split between two components: interest (the lender's fee for lending you money) and principal (actual reduction of the balance you owe). Understanding how car financing works starts with understanding this split — because it's not 50/50, and it doesn't stay constant.

In the early months of a car loan, the vast majority of each payment goes to interest. In the final months, the opposite is true — almost all of each payment goes to principal. This is front-loading, and it's a fundamental feature of how amortizing loans work. It's not unique to auto loans; mortgages work the same way. But because car loans involve depreciating assets (unlike real estate), the front-loaded interest has much more dramatic consequences for your equity position.

The practical effect: you build equity in your vehicle much more slowly than you'd expect based on the payment size alone. A payment that feels substantial actually chips away at the balance modestly in year one, then more aggressively in year three and beyond. This is why understanding how car loan payments work changes how most people think about term length.

The Math: A Sample Amortization Table

Let's make this concrete. Here's a real-world example: a $20,000 loan at 14.99% annual interest rate, paid biweekly over 72 months (156 payments). This is a realistic scenario for a subprime or near-prime borrower in Alberta financing a reliable used vehicle.

First, the biweekly payment: approximately $247. That's 156 payments of $247 = $38,532 total paid — meaning you'll pay $18,532 in interest over the life of this loan on a $20,000 vehicle.

| Payment # | Period | Payment | Interest Portion | Principal Portion | Balance Remaining |

|---|---|---|---|---|---|

| 1 | Biweek 1 | $247 | $115 | $132 | $19,868 |

| 6 | Month 3 | $247 | $114 | $133 | $19,207 |

| 26 | Month 13 | $247 | $108 | $139 | $17,768 |

| 52 | Month 25 | $247 | $98 | $149 | $15,941 |

| 78 | Month 37 | $247 | $86 | $161 | $13,872 |

| 104 | Month 49 | $247 | $72 | $175 | $11,413 |

| 130 | Month 61 | $247 | $55 | $192 | $8,515 |

| 156 | Month 72 | $247 | $1 | $246 | $0 |

See what's happening? In payment #1, you're paying $115 in interest and only $132 toward the actual balance. The interest portion is 46% of your total payment. At payment #104 (month 49), the interest portion has dropped to $72 — but that's still 29% of every payment going to the lender rather than building your equity. Only in the final stretch do payments tip heavily in your favour.

This table also reveals something important: after 25 months of faithful biweekly payments (52 payments), you still owe nearly $16,000 on a $20,000 loan. You've paid roughly $12,800 in total — but only about $4,000 went to the principal. The rest was interest. That's the math that creates negative equity during the years when vehicles depreciate fastest.

How Your Interest Rate Changes Everything

The rate you receive on your loan doesn't just affect the payment amount — it dramatically changes the interest-to-principal split on every single payment. Compare three borrowers all taking a $20,000 loan over 72 months:

| Rate | Biweekly Payment | Total Paid | Total Interest | Interest % of Total |

|---|---|---|---|---|

| 6.99% | $214 | $33,384 | $13,384 | 40% |

| 14.99% | $247 | $38,532 | $18,532 | 48% |

| 24.99% | $285 | $44,460 | $24,460 | 55% |

The difference between 6.99% and 24.99% on a $20,000 loan is $11,076 in total interest over 72 months. That's more than half the original loan amount paid in additional interest cost. This is why the rate you're offered in Alberta matters so much, and why improving your credit situation — even modestly — before applying can save you thousands. The variable vs. fixed rate question also deserves attention; the guide on variable vs. fixed rate car loans in Alberta breaks down when each makes sense.

Why Shorter Terms Save Dramatically More Than You'd Think

Most people look at loan term as a simple payment-size lever: longer term equals smaller payment. True. But the compounding effect on total interest paid is far more dramatic than the payment difference suggests.

| Term | Biweekly Payment | Total Paid | Total Interest | vs. 48-month |

|---|---|---|---|---|

| 48 months | $299 | $28,704 | $8,704 | — |

| 60 months | $261 | $31,320 | $11,320 | +$2,616 |

| 72 months | $247 | $38,532 | $18,532 | +$9,828 |

| 84 months | $233 | $43,344 | $23,344 | +$14,640 |

| 96 months | $227 | $47,664 | $27,664 | +$18,960 |

(All calculations based on $20,000 loan at 14.99% annual rate)

Let that sink in: going from a 48-month term to a 96-month term saves you about $72 biweekly — but costs you $18,960 in additional interest. You're trading less than $75 per payment for nearly nineteen thousand extra dollars in total cost. It feels like a good deal in the moment. The amortization math says otherwise.

More practically: that $72 in monthly savings buys you a severely worse equity position throughout the loan, more years of insurance and maintenance costs on a vehicle you technically don't own, and less financial flexibility if circumstances change. The biweekly payment structure already accelerates paydown compared to monthly — pairing it with a shorter term maximizes the benefit. Use our payment calculator to model your own numbers and see the total-paid comparison across terms before deciding.

How Extra Payments Change the Amortization Curve

Here's where amortization actually works in your favour, if you know how to use it. When you make an extra payment directly to principal — even a small one — you're skipping ahead on the amortization schedule. You're paying off amounts that would otherwise generate months of future interest charges.

Back to our $20,000 loan at 14.99% over 72 months. Regular payment: $247 biweekly. Now add just $50 extra per payment, applied to principal:

- Regular payments only: 72 months, $18,532 in total interest

- Extra $50/payment to principal: Approximately 62 months, ~$15,800 in total interest

- Savings: ~10 months shorter, ~$2,700 saved in interest

An extra $50 per biweekly payment — about the cost of a nice dinner — cuts 10 months and $2,700 off the loan. That's leverage. And because you're compressing the front-loaded interest phase, you build equity faster, exit the negative equity window sooner, and have more flexibility if you need to sell or trade. For a deeper look at whether early payoff makes sense for your situation, the complete math on paying off your car loan early covers the tradeoffs in detail.

Important: confirm with your lender that extra payments apply directly to principal rather than simply advancing your next payment date. Most Canadian auto lenders handle this correctly, but it's worth verifying. The accelerated car payments page explains how this works with different lender structures.

Biweekly vs. Monthly Payments: The Hidden Advantage

Most Canadian auto lenders default to biweekly payments, and there's a structural reason: biweekly payments create a natural extra payment each year. There are 26 biweekly periods in a year, which equals 13 monthly payment equivalents — one extra month's worth of payments annually compared to a strict 12-payment monthly schedule.

On our $20,000 loan example, that extra annual payment quietly chips away at the principal every year, slightly compressing the amortization schedule. It's not as dramatic as deliberately adding extra payments, but it's a free benefit built into the biweekly structure that you get without changing your behaviour at all.

How a Rate Drop Reshapes Your Entire Amortization Schedule

Refinancing a car loan to a lower rate doesn't just reduce your biweekly payment — it restructures every single payment in the new schedule. When the interest rate drops, the interest portion of each payment shrinks, which means more of each dollar goes to principal from payment one onward. The cumulative effect is significant.

Here's a concrete before-and-after. Suppose you took out a $20,000 loan at 19.99% over 72 months. Eighteen months in, your credit has improved — you've made all your payments on time, maybe cleared some other debt — and you qualify to refinance the remaining balance at 13.99%.

- Original loan at 19.99%: Biweekly payment ~$283. Total interest over 72 months: ~$24,376.

- Remaining balance at month 18: Approximately $17,900 (most early payments went to interest, remember).

- Refinanced at 13.99% over remaining 54 months: New biweekly payment ~$228. Total remaining interest: ~$6,500.

- Estimated interest saved by refinancing: $3,500 to $4,500 over the remaining term.

That's a meaningful saving achieved simply by asking the question and having an improved credit profile to back it up. The refinance also changes the character of every remaining payment: a higher fraction goes to principal, which means you build equity faster and exit the negative equity window sooner. If your credit situation has improved since you took out your original loan — which is common after 12-24 months of on-time payments — it's worth exploring car loan refinancing in Alberta to see what rate improvement you qualify for now.

The Amortization Math in Subprime Financing: What to Expect

Understanding amortization is especially important for subprime borrowers, because the combination of higher rates and longer terms means the front-loading of interest is more pronounced. If your lender is offering you a 96-month loan at 22.99% on a $20,000 vehicle, the amortization math looks dramatically different than a 48-month loan at 7.99%.

On that 96-month, 22.99% loan:

- Biweekly payment: approximately $236

- Total paid: $36,816

- Total interest: $16,816 — 84% of the original loan amount in interest

- After 24 months, you've paid $11,328 in total payments but reduced the principal by only about $2,400

This isn't a reason not to finance — reliable transportation is not optional for most working Albertans. But it is a reason to treat the loan as something to actively manage rather than passively carry. Even small interventions — $30 extra per payment, a $500 lump sum when tax season comes — have outsized effects early in a high-rate long-term loan because you're cutting into the most interest-heavy portion of the amortization schedule.

Subprime financing is a tool for accessing transportation when your credit situation makes conventional rates unavailable. The goal is to use it, rebuild your credit through consistent payments, and then refinance to a better rate or replace the vehicle with better-structured financing the next time. It's a stepping stone, not a permanent state. The connection between car payments and credit rebuilding is part of what makes auto financing a useful tool for improving your financial profile — even when the initial rate is higher than you'd like.

What Amortization Means for Your Equity Position

Amortization and equity are two sides of the same coin. Your equity in the vehicle at any point is: current market value minus outstanding loan balance. Since the outstanding balance drops slowly in the early months (because most payments go to interest), and the vehicle depreciates quickly in those same months, most borrowers are in negative equity for the first two to four years of a typical loan — especially with longer terms.

If you're concerned about negative equity or want to understand where you currently stand, the complete guide to negative equity car loans walks through how to check your position and what to do about it. It pairs directly with this amortization math to give you the full picture.

For vehicles with strong resale value — like the Honda CR-V, which holds its value well in Alberta's crossover market — the equity crossover point comes sooner because the vehicle depreciates less steeply than the average. This is one of the underappreciated arguments for buying a vehicle with strong resale: it's not just about what you get when you sell, it's about how quickly you build real ownership stake throughout the loan.

Reading Your Loan Statement

Your monthly or biweekly statement from the lender should break out each payment into its interest and principal components. If it doesn't, call and ask — or request a full amortization schedule. You're entitled to this information, and reputable lenders provide it without pushback.

What you're looking for:

- Current balance (how much you still owe)

- Interest charged this period (what went to the lender)

- Principal paid this period (what reduced your balance)

- Next payment date

Tracking these numbers monthly — even just glancing at the split — builds financial literacy that serves you well beyond the vehicle you're currently financing. You'll start to see the crossover point approaching as the principal portion grows and interest shrinks. That crossover is your equity milestone: the point where principal payments exceed interest payments, meaning you're building real ownership faster than you're paying for borrowed money.

How to Use This Knowledge When Buying

When you're in the finance office, you now know what questions to ask:

- "Can you show me the full amortization table for this loan?"

- "What's the total interest I'll pay over the life of the loan at this rate vs. a shorter term?"

- "If I make extra principal payments, how does that change my payout timeline?"

- "Is there any prepayment penalty if I pay this off early?"

These questions signal that you understand the math and aren't making a decision based on biweekly payment alone. They also move the conversation toward the numbers that actually matter for your long-term financial health.

The most common mistake buyers make in the finance office is optimizing for the smallest biweekly payment number without asking what that number costs them in total. A dealer who shows you only the payment — "just $199 every two weeks!" — isn't lying, but they're showing you the least useful number for making a smart decision. The total interest paid over the full term is the number that actually measures what the loan costs you. Always ask for it.

A second useful perspective: what does the vehicle cost you per kilometre over the ownership period? If you drive 20,000 km/year and own the vehicle for 5 years, that's 100,000 km of use. A vehicle that costs $20,000 in principal plus $18,532 in interest equals $38,532 total — about $0.39 per kilometre just in financing costs, before fuel, insurance, or maintenance. Framing the loan this way connects the abstract amortization math to the real-world utility you're getting from the vehicle. A lower-rate, shorter-term loan on the same vehicle at the same price might cost $28,700 total — $0.29 per kilometre. The difference is $0.10 per kilometre, or about $10,000 over that ownership period.

If you're in the Airdrie area and want to work through these numbers with a team that presents them transparently — full amortization schedule, total interest paid, rate comparison across lenders — that's exactly how we work with every customer. No surprises at delivery, no payment-only conversations.

Ready to see how amortization applies to your specific situation? Start your financing application and our team will model the numbers — showing you exactly where your payments go and what different terms cost you over the full loan life.

Compare and Apply

- Subprime Auto Financing Explained — car loan rates by credit tier

Financing Resources

Related Articles

Ready to Find Your Vehicle?

Browse our inventory or apply for financing. All credit situations welcome.

★★★★★ 96+ Google Reviews · AMVIC Licensed · Free Delivery 300km