How Car Loans Build Credit: A Month-by-Month Timeline

In this article

- The Credit Score Fundamentals You Need First

- Month 1-3: The Dip You Need to Expect

- Month 4-6: Stabilization and the First Real Movement

- Month 7-12: The Steady Climb Begins

- Year 2: The Meaningful Threshold Crossing

- How the Two Credit Bureaus Report Differently

- Maximizing the Credit-Building Effect: What to Do Alongside the Loan

- Pay Biweekly Instead of Monthly

- Set Up Automatic Payments

- Handle Any Outstanding Collections

- Don't Close Old Accounts

- Refinancing: The Month-18 Opportunity

- What This Looks Like in Practice

- Common Mistakes That Stall or Reverse Credit Progress

- Paying Late "Just Once"

- Opening Multiple New Credit Accounts

- Co-Signing Without Understanding the Risk

- How Lenders View Your Credit Profile After 12-24 Months

- Related Buyer Guides

- Compare and Apply

Check Your Options in 3 Minutes

No credit impact. All credit situations welcome.

★★★★★ 89+ Google Reviews · AMVIC Licensed · Free Delivery 300km

If your credit score is sitting below 600 and someone tells you a car loan will help rebuild it, your first reaction might be skepticism. Doesn't taking on debt make things worse? Won't another inquiry drop your score further? These are reasonable questions — and the answer is more nuanced than either "yes it helps" or "no it hurts." The truth is that a car loan is a precision instrument for credit rebuilding when used correctly, and the month-by-month timeline of what actually happens to your score is something most people have never seen laid out concretely. This post does exactly that.

See what you pre-qualify for

Three quick answers — soft check, no commitment.

The Credit Score Fundamentals You Need First

Before the timeline makes sense, you need to understand what actually moves your credit score. Canada uses two main credit bureaus — Equifax and TransUnion — and both use similar (though not identical) scoring models. The five factors that determine your score, roughly in order of weight:

- Payment history (~35%): Have you paid on time? This is the single biggest factor. One missed payment can drop a score by 50-100 points depending on the severity.

- Credit utilization (~30%): How much of your available revolving credit (credit cards, lines of credit) are you using? Under 30% is good. Under 10% is excellent. This factor is irrelevant for installment loans like car loans.

- Length of credit history (~15%): Older accounts help your score. New accounts temporarily hurt it.

- Credit mix (~10%): Having a healthy mix of installment loans (car loan, mortgage) and revolving credit (credit cards) signals creditworthiness. If you only have credit cards, adding an installment loan improves your mix.

- New credit inquiries (~10%): Each hard inquiry drops your score by a few points temporarily. Multiple inquiries in a short window for the same type of loan are treated as rate shopping and typically counted as one.

A car loan primarily impacts payment history (massively), credit mix (positively), length of history (initially negative, then positive), and new inquiries (briefly negative). For a deeper foundation, how credit scores work in Canada covers the full scoring model in detail.

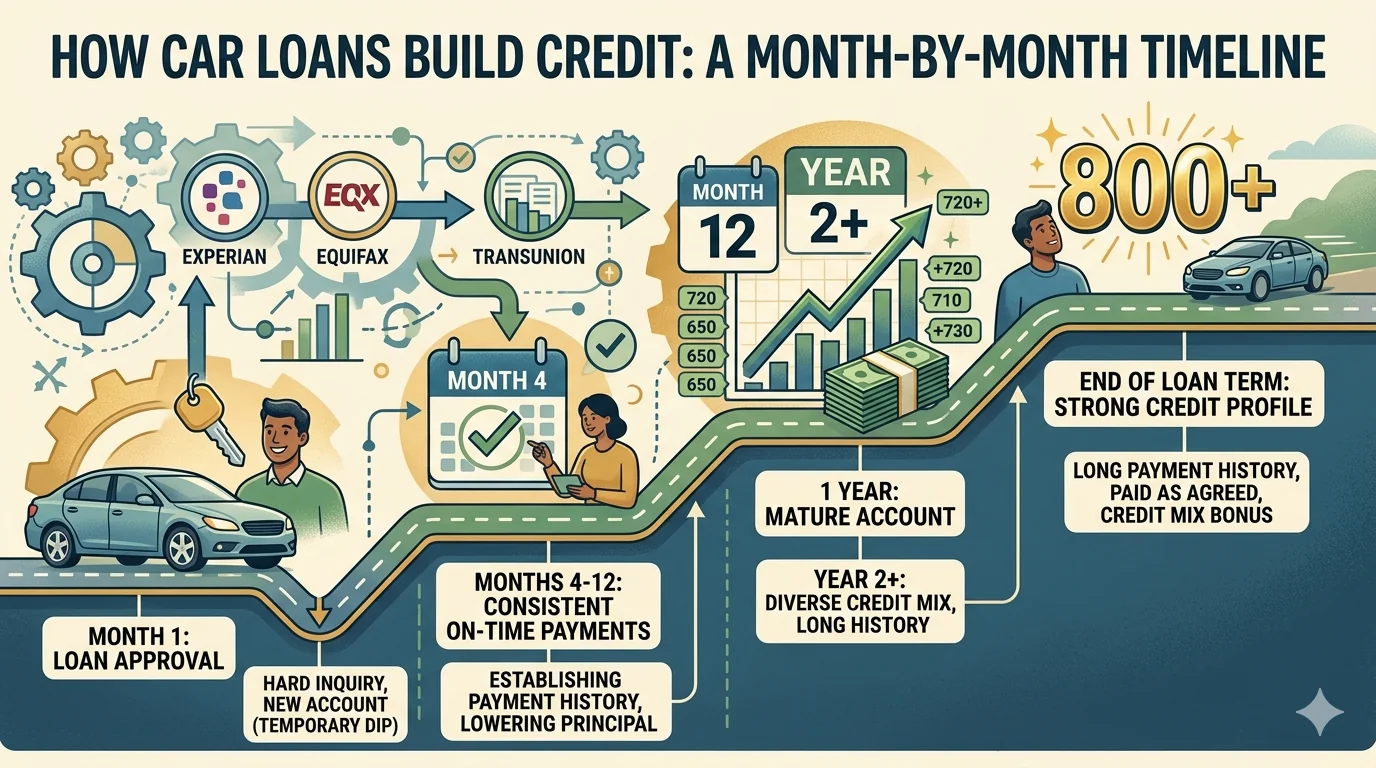

Month 1-3: The Dip You Need to Expect

Here's what no one tells you upfront: your credit score will likely drop in the first one to three months after taking out a car loan. Not because the loan is hurting you — but because the short-term mechanics of how new credit is reported create a temporary score decrease.

What happens in month one:

- The hard inquiry from your application registers: -5 to -10 points, depending on your score and existing inquiry history

- A new account with a large balance appears: -5 to -15 points (new accounts temporarily lower average age of credit history and appear as new risk)

- The loan balance is at 100% of the original amount — the highest it will ever be: modest negative impact on some scoring models

Starting example: if your score is 550 when you sign, don't be alarmed to see it at 530-540 at your first check three to four weeks later. This is normal. The critical thing to understand is that this dip is front-loaded — it's all the negative impacts landing at once, with no positive payment history yet to counterbalance them. The recovery begins as soon as month two or three, as your first on-time payments report.

The short-term dip is the entry fee. The years of positive payment history are the return. Don't make the mistake of checking your score in month two and concluding the loan isn't working.

During this window: make your first one to two payments on time and don't miss them for any reason. Payment history begins reporting immediately, and a missed payment this early would extend the negative phase significantly.

Month 4-6: Stabilization and the First Real Movement

By month four, your credit report now shows two to three consecutive on-time payments. This is when the score stops dropping and begins stabilizing — often recovering the inquiry-driven dip and starting to creep upward.

Realistic trajectory for a 550 starting score:

| Milestone | Estimated Score | Primary Driver |

|---|---|---|

| Loan signed (Month 0) | 550 | Starting point |

| Month 1-2 | 530-540 | Hard inquiry + new account opening |

| Month 3 | 540-550 | First payments reporting, partial recovery |

| Month 6 | 555-570 | Consistent payment history accumulating |

| Month 12 | 580-600 | 12 months of perfect payment history |

| Month 18 | 610-640 | Account aging + continued payment history |

| Month 24 | 640-670+ | Near-prime territory, loan balance meaningfully reduced |

These numbers are illustrative — actual score movement depends on your full credit profile, any negative items aging off your report, and whether you're adding or damaging credit elsewhere during this period. Someone with only one negative item on their report will often see faster improvement than someone with multiple collections still active.

Month four through six is also when lenders start seeing a pattern. The first few payments have the highest signal value — lenders know that people who default usually do so in the first six months. Making it to six consecutive on-time payments significantly improves your standing for future credit applications. This is why first car loans for credit building are such an effective tool — six months of disciplined payments opens doors that were closed before.

Month 7-12: The Steady Climb Begins

This is where the car loan's credit-building power really becomes visible. By month seven, you have a full six months of payment history. By month twelve, you've demonstrated a year of responsible installment loan management. For someone who entered with a 550 score — likely the result of missed payments, collections, or limited credit history — a year of perfect car loan payments is substantial positive evidence.

The practical effect: scores in the 580-600 range after 12 months means you've crossed from deep subprime into subprime territory. That matters for future credit applications — credit cards become more accessible, you may qualify for lower-rate refinancing on the car loan itself, and landlords running credit checks will see a different picture than a year ago.

During this window, be deliberate about protecting the progress. Common mistakes in months 7-12 that erase gains:

- Missing a single payment — payment history damage is asymmetric; one miss can wipe several months of progress

- Maxing out credit cards while the car loan is active — high utilization drags scores down even as payment history improves

- Applying for multiple new credit products — stacking inquiries during the rebuilding phase slows the climb

- Co-signing for someone else's loan — their payment behavior now affects your score directly

What to do instead: if you don't have a credit card, add one secured card with a low limit and keep the balance under 30%. This adds a revolving credit account to your mix and compounds the score improvement from the car loan. Don't open multiple cards — one is enough to improve your credit mix without creating inquiry damage or utilization risk.

Year 2: The Meaningful Threshold Crossing

If you've maintained every payment on time through month 24, several things happen simultaneously that accelerate score improvement:

Account age: The car loan is now two years old. It's contributing positively to your average age of credit history rather than dragging it down as a "new" account. If you had no credit history before the loan, you now have a two-year-old account — a meaningful foundation.

Balance reduction: On a 72-month loan, you're roughly one-third of the way through. The balance is meaningfully lower than the original amount. Some scoring models factor loan-to-original-amount ratio, and a declining balance reads as responsible debt management.

Negative item aging: Negative items on your credit report have less impact over time. A collection from three years ago affects your score less than a collection from last year. If the negative items that created your 550 score were from two or more years ago, they're now aging off in impact (though they remain on the report for 6-7 years in Canada).

The realistic outcome after 24 months of perfect payment on a car loan: a score that started at 550 is often sitting at 640-670+. That's the near-prime range — meaningfully better financing rates, credit card approvals without secured card requirements, and a credit profile that reflects the person you are now rather than the circumstances of years ago.

For a detailed look at the full timeline including what happens beyond 24 months, the credit rebuilding timeline guide maps the full journey from subprime to prime.

How the Two Credit Bureaus Report Differently

Equifax and TransUnion both receive reports from lenders — but not every lender reports to both, and reporting timelines vary. Most major lenders in Canada report to both bureaus, but some specialty and subprime lenders report to only one. This creates a common scenario: your Equifax score and TransUnion score differ noticeably, sometimes by 20-40 points.

For the car loan credit-building strategy, this matters in two ways:

- When you check your score to monitor progress, check both bureaus. Borrowell uses Equifax; Credit Karma uses TransUnion. Both are free. The one a specific lender checks determines which score matters for that application.

- If your car loan lender only reports to one bureau, you'll see asymmetric improvement. The loan will be building your score on one bureau but not appearing on the other. This is normal and expected — not a sign something is wrong.

You can access both reports for free through free credit score checking options in Canada. Do this quarterly during your rebuilding period — not monthly. Checking your own score is a "soft inquiry" that has zero impact on your score, but obsessing over small fluctuations creates anxiety without actionable insight. Quarterly is enough to track meaningful progress.

Maximizing the Credit-Building Effect: What to Do Alongside the Loan

A car loan alone is a single-track approach. These parallel actions compound the improvement:

Pay Biweekly Instead of Monthly

Most car loans in Alberta are structured with biweekly payments, which Shift Happens uses by default. Biweekly payments mean 26 payment periods per year rather than 12. You make the equivalent of one extra monthly payment per year, which reduces your principal faster and shortens the loan term. Less interest paid, loan balance reduces faster — both positive effects.

Set Up Automatic Payments

The single biggest risk to your credit-building plan is a missed payment. One missed payment undoes months of progress. Autopay eliminates the human error risk entirely. Your score improvement is now protected from forgetfulness, busy weeks, or banking delays.

Handle Any Outstanding Collections

Collections that remain open on your report continue damaging your score regardless of how well you're paying the car loan. If you have active collections under $5,000, consider negotiating settlements during your rebuilding period. A settled collection still appears on your report, but the damage decreases over time. A collection paid in full ideally gets marked "paid" — call the collector before paying to negotiate removal if possible.

Don't Close Old Accounts

If you have old credit cards — even ones with bad history — don't close them during the rebuilding period. Closing accounts reduces your available credit limit (hurting utilization) and removes account age from your average. Keep them open with zero balance. The negative history ages off eventually; the account age benefit is permanent.

For more on parallel strategies that work alongside a car loan, rebuilding credit with a car loan covers the full playbook.

Refinancing: The Month-18 Opportunity

Here's something many credit rebuilders don't know: if your car loan was originated at a higher rate due to subprime credit — say 19.99-24.99% — and you've made 18 months of perfect payments, you may qualify to refinance at a meaningfully lower rate. Lenders looking at an applicant with 18 consecutive on-time payments and a score that's climbed from 550 to 620+ see a very different risk profile than they saw at the original application.

Refinancing at month 18 from 24.99% to 14.99% on a remaining $18,000 balance over 42 remaining months saves approximately $2,800 in interest over the loan term — and the lower payment can free up cash to pay down other debts or build the emergency fund that protects your credit-building progress.

Refinancing does add a new hard inquiry and resets some of the account-age clock, so it's a trade-off. But for high-rate loans where the interest savings are significant, it's worth evaluating. How car payments build credit covers the refinancing decision in more detail.

What This Looks Like in Practice

Consider a scenario: someone in Calgary comes to us with a 555 credit score — a previous consumer proposal that was discharged 18 months ago, one credit card with no negative history, and stable employment income. We structure them into a 2020 Honda Civic at $16,500 with a $2,000 down payment. The loan is $14,500 at 19.99% over 72 months — $186 biweekly.

Eighteen months later: score is 615. They return and we refinance to 13.99% on the remaining $11,800 balance — dropping the payment to $152 biweekly and saving them $1,900 in remaining interest. By month 36, score is 645. By loan completion at month 72, score is likely near-prime or prime — and they've built three years of documented payment history on a major installment loan. The next car loan, mortgage application, or business line of credit will have a completely different starting point than that first application.

This is the arc the car loan credit-building strategy is designed to deliver. It takes patience and consistency — but the math works, and the timeline above is what you can realistically expect.

Common Mistakes That Stall or Reverse Credit Progress

The credit-building arc described above assumes consistent, disciplined behavior throughout the loan term. In practice, life happens — and certain common mistakes can stall or reverse the progress you've built, sometimes significantly. Knowing these in advance is the best way to avoid them.

Paying Late "Just Once"

Payment history is reported in binary terms: paid on time, or didn't. There is no partial credit for "usually on time." A single 30-day late payment — even on an account that's been perfect for a year — can drop your score by 60-100 points depending on your current score and credit profile. Higher scores actually take larger point hits from a single late payment because there's more to lose. If you ever find yourself in a month where you genuinely can't make a payment, call the lender before the due date. Many lenders, especially subprime-focused ones, have hardship deferral programs. A deferred payment arranged in advance doesn't report as late; a missed payment does.

Opening Multiple New Credit Accounts

Once you're 12 months into your car loan and seeing score improvement, there's a tempting trap: retailers, banks, and credit card companies start approving you for things they wouldn't have before. Every new account is another hard inquiry and another "new account" impact. Opening three credit cards in month 14 of your rebuilding journey can push your score back down by 30-50 points temporarily — undoing six months of progress. Be selective. One new credit product at a time, spaced at least 6 months apart, is the disciplined approach.

Co-Signing Without Understanding the Risk

Once your credit improves, friends and family may ask you to co-sign their loans. This is an enormous decision. As a co-signer, their payment history reports on your credit file. If they miss payments — even consistently — your score suffers. And you are legally responsible for their debt if they stop paying. Your rebuilt credit can be destroyed by someone else's financial struggles. Co-signing is a generosity that can cost you years of credit-rebuilding work. Decline unless you would be fully comfortable making every single payment on that loan yourself.

How Lenders View Your Credit Profile After 12-24 Months

The credit score number gets most of the attention — but experienced lenders, especially in the subprime and near-prime space, look at the full tradeline history, not just the score. Understanding what they actually see helps you understand why consistent payment history matters beyond the numerical score impact.

After 24 months of perfect car loan payments, your credit profile shows:

- A 24-month installment loan with zero late payments — the highest-quality type of payment history

- A loan balance that has declined from the original amount, demonstrating active paydown

- An account that's now two years old — old enough to contribute positively to credit history length

- No recent hard inquiries if you've been disciplined about new credit applications

A lender reviewing this profile — for a refinance, a mortgage application, or a new car loan — sees someone who has demonstrated sustained financial discipline over a two-year period. That's fundamentally different from what a score alone communicates. A 640 score built through 24 months of car loan payments reads very differently to an experienced underwriter than a 640 score with a spotty payment history and recent collections. The provenance of the score matters.

This is also why subprime lenders often look at "time since last derogatory" — how long ago your last negative item occurred. Two years of clean payment history after a rough period is a strong signal. It doesn't erase the past, but it provides compelling counter-evidence that the risk has changed.

If you're considering using a car loan to rebuild your credit, check whether you'd qualify with our quick assessment tool — no hard inquiry, just a realistic read on your options. Or go straight to our financing application to see what our lenders can structure for your situation. We specialize in working with all credit situations across Alberta, including international students building credit for the first time — if that's your situation, our guide for international students building credit with a car loan is specifically written for you.

Before you apply, pulling and reviewing your own credit report is a smart first step. Our walkthrough on how to read your Equifax report before applying for a car loan shows you exactly what lenders see and what to look for.

Compare and Apply

- Bad Credit Financing — Complete Guide — subprime auto financing options

Financing Resources

Related Articles

Ready to Find Your Vehicle?

Browse our inventory or apply for financing. All credit situations welcome.

★★★★★ 89+ Google Reviews · AMVIC Licensed · Free Delivery 300km