Untangling Joint Car Loans After Separation in Alberta

In this article

- Why Joint Car Loans Are Complicated During Separation

- Vehicles as Matrimonial Assets in Alberta

- Your Three Main Options

- Option 1: One Party Assumes the Loan (Requires Refinancing)

- Option 2: Sell the Vehicle and Split the Proceeds

- Option 3: Trade In and Each Get Separate Vehicles

- How Separation Affects Your Credit

- Your Legal Obligations Until the Loan Is Restructured

- Protecting Your Credit Through the Process

- Getting Your Own Vehicle After Separation

- Income Documentation Changes

- Credit Rebuilding for Post-Separation Borrowers

- Practical Vehicle Choices After Separation

- Common Misconceptions About Joint Car Loans and Separation

- What to Expect When Refinancing During Separation

- A Note on Timing

- Related Buyer Guides

- Compare and Apply

Check Your Options in 3 Minutes

No credit impact. All credit situations welcome.

★★★★★ 89+ Google Reviews · AMVIC Licensed · Free Delivery 300km

You and your partner are splitting up, and somewhere in the middle of lawyers, emotions, and dividing up the furniture is a car loan with both your names on it. Nobody warned you that the vehicle sitting in the driveway could become one of the most complicated parts of the whole separation. In Alberta, a jointly financed vehicle isn't just a transportation problem — it's a legal and financial problem that can follow both of you for years if you don't handle it properly.

See what you pre-qualify for

Three quick answers — soft check, no commitment.

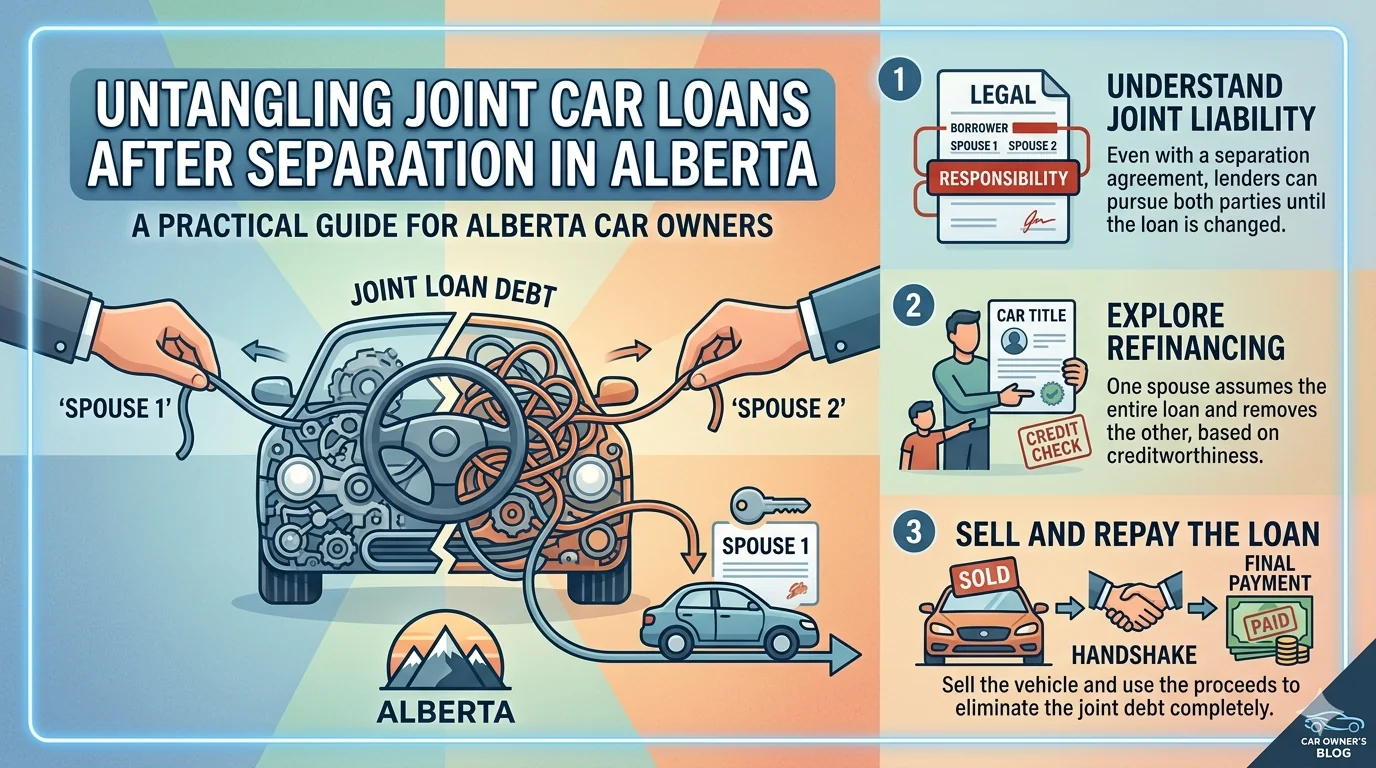

Why Joint Car Loans Are Complicated During Separation

When two people sign a car loan together, the lender doesn't care what happens between them personally. Both parties remain 100% liable for the full debt — not 50/50, but each of you fully responsible. That means if your ex stops making payments, the lender will come after you. If the vehicle gets repossessed, it shows on both credit files. The separation agreement you sign with a lawyer carries legal weight between the two of you, but it means nothing to the bank.

This is the part most couples learn the hard way. A separation agreement that says "he gets the truck" doesn't remove her name from the loan. Until the loan is formally restructured or paid off, both names remain on the liability. Missing even a single payment during a dispute can knock 60-100 points off both your credit scores — at exactly the moment when you're both about to need financing for new housing, new vehicles, and a fresh start.

Alberta's Matrimonial Property Act treats vehicles purchased during the relationship as matrimonial property, subject to equitable division. That doesn't automatically mean 50/50 — it means the courts consider each party's contribution, who has been using the vehicle, outstanding loan obligations, and the vehicle's net equity (market value minus what's owed). Knowing where you stand legally before you make any moves is essential.

Vehicles as Matrimonial Assets in Alberta

Under the Matrimonial Property Act, any vehicle acquired during the marriage (or in some cases, during cohabitation if you have a cohabitation agreement) is considered matrimonial property. Vehicles owned before the relationship started are generally exempt — but any appreciation in value during the marriage may still be divided.

For practical purposes, most separating couples are dealing with one of three scenarios:

- One vehicle, both names on the loan. Most common, most complicated.

- One vehicle, one name on the loan, but acquired during the marriage. The vehicle is still matrimonial property even if only one person is on the loan.

- Two vehicles, each in different names. Simpler to divide, but equity differences between the two vehicles may require a payment from one party to the other.

The net equity position of the vehicle matters enormously. If you owe $28,000 on a vehicle worth $32,000, there's $4,000 in equity to divide. If you owe $28,000 on a vehicle worth $22,000, you're looking at $6,000 in negative equity — and now both parties are sharing a liability, not an asset. A realistic appraisal of the vehicle's current market value is the starting point for any negotiation.

Your Three Main Options

Option 1: One Party Assumes the Loan (Requires Refinancing)

The cleanest long-term solution is for one person to refinance the vehicle entirely in their own name, paying out the existing joint loan and replacing it with a new loan solely in their name. This removes the other party from both the title and the financial obligation.

This is not a simple paperwork change. The lender must agree to release one party, and most lenders will not simply remove a co-borrower — they require a full new credit application. The person assuming the loan must qualify independently based on their income, credit score, and debt ratios. Refinancing a car loan in Alberta during separation works the same way as any refinance: new application, new credit pull, new approval decision.

The challenge is that separation itself can affect your financial picture. Income may have changed. You may have moved out and have new housing costs. Your debt-to-income ratio looks different as a single-income household. Lenders who specialize in real-life credit situations — rather than just approving people who need no help — are often better positioned to work through the new numbers with you.

Option 2: Sell the Vehicle and Split the Proceeds

If neither party can qualify to assume the loan alone, or if neither wants the vehicle, selling it and splitting whatever equity remains (after paying off the loan) is a straightforward exit. Both parties sign off on the sale, the loan gets paid out from the proceeds, and each person walks away with their share.

The complications arise when there's negative equity — you owe more than the vehicle is worth. In that case, both parties need to come up with the shortfall before the sale can close. Who pays that difference is a negotiation point, and it often needs to be spelled out in the separation agreement.

Timing matters with this option. If you're considering selling through a dealership trade-in, understand that trucks and larger SUVs have been holding their value relatively well. A formal appraisal of your vehicle's current worth — before you negotiate — gives you a real baseline rather than an emotional number.

Option 3: Trade In and Each Get Separate Vehicles

Some couples find that the most practical resolution is to trade in the joint vehicle and use the proceeds to help each party get into their own separate vehicle. This works especially well when there's meaningful equity in the joint vehicle.

For example: a $35,000 truck with a $20,000 remaining loan has $15,000 in equity. Trade it in, split the $15,000 proceeds, and each party now has a $7,500 down payment toward their own vehicle. Two smaller, more affordable vehicles might actually improve both parties' monthly financial situations compared to the original joint vehicle payment.

This approach also sidesteps the refinancing qualification problem — rather than one person needing to qualify for the full existing loan, each person is applying for a smaller, more manageable loan on a vehicle they chose for their new life circumstances.

How Separation Affects Your Credit

The credit damage that happens during separations is often preventable, but it requires both parties to act deliberately and sometimes cooperate even when that's the last thing they want to do.

The most common credit problems during separation:

- Missed payments during disputes. If neither party is sure who's responsible for the car payment while negotiations drag on, and both assume the other is handling it — the payment goes missed. The lender reports it to Equifax and TransUnion, and both credit scores take the hit.

- Spite decisions. In contentious separations, one party may stop making payments on purpose, knowing it will damage the other's credit. This is self-defeating — it damages their own credit just as much.

- Account confusion. Joint accounts sometimes get caught in account freezes or disputes, causing automatic payments to fail even when both parties intended to pay.

Key protection: Until the vehicle loan is formally restructured, keep paying it — even if you're in a dispute about who should ultimately be responsible. Document everything. A $450 missed payment that causes a 90-point credit drop will cost you far more in higher interest rates on your next vehicle than whatever you were trying to withhold. Deal with the dispute through lawyers; keep the lender happy in the meantime.

If your credit has already taken damage during a difficult separation, you're not alone — and you're not stuck. Rebuilding credit with a car loan is a well-documented path back, and lenders who specialize in credit recovery situations can often work with scores well below what traditional banks require.

Your Legal Obligations Until the Loan Is Restructured

This is the part that catches people off guard: your legal obligations to the lender exist completely independently of your legal obligations to your ex-spouse.

A separation agreement is a contract between you and your former partner. It does not modify or replace the contract between both of you and the lender. If your separation agreement says your ex is responsible for the car payment and they don't pay, the lender will still report you to the credit bureau and pursue collections against you. Your only recourse at that point is to sue your ex for breach of the separation agreement — which is an expensive, slow process that doesn't repair your credit in the meantime.

This is why restructuring (refinancing or selling) the loan as quickly as possible after separation is in both parties' financial interest. Every month that joint loan stays open is another month of shared liability risk.

If you're concerned about a jointly held vehicle loan that your ex has control of, you have a few protective options:

- Set up your own payment directly with the lender (some will allow this on joint loans).

- Ask your lawyer to include a specific clause in the interim separation agreement about vehicle payment responsibility, with indemnification provisions.

- Move quickly toward a permanent resolution (refinance, sale, or trade).

Protecting Your Credit Through the Process

Your credit score going into the separation affects your options coming out of it. If you can exit the marriage or common-law relationship with your credit intact, you're in a dramatically stronger position to rebuild your financial life independently. Rebuilding your credit with a car loan is possible even if some damage has already occurred — but protecting what you have is always preferable.

Practical steps to protect your credit during separation:

- Pull your free credit report immediately. Know exactly where you stand — what accounts are jointly held, what's reporting, and what your current scores are on both Equifax and TransUnion.

- Contact every lender with a joint account. Inform them of the separation and ask what options exist — some will flag the account, change payment arrangements, or document your contact.

- Don't close joint accounts in anger. Closing a joint credit account can actually hurt your credit by reducing your available credit. The goal is to separate or transfer the account, not simply close it.

- Keep your own accounts current. Pay everything you are personally responsible for, on time, every time. Your personal payment history is the most powerful lever you have.

Getting Your Own Vehicle After Separation

At some point — whether it's through the resolution of the joint vehicle situation or a new purchase — you'll need your own vehicle. This is where many newly separated Albertans run into unexpected friction.

Income Documentation Changes

One of the most common post-separation financing challenges is income documentation. A two-income household that qualified easily for a loan may look completely different when one income has to carry the full picture. Additionally, if you've changed jobs, reduced hours, or moved to a different employment type during or after the separation, lenders need to see your current income clearly.

If you've recently started a new job post-separation, some lenders have restrictions on approving borrowers in probationary periods. Others work with the full context of your situation. Having two to three months of recent pay stubs, your employment letter, and your most recent T4 ready will speed the process considerably.

Credit Rebuilding for Post-Separation Borrowers

If your credit score took hits during the separation process, you're not out of options. Lenders who specialize in non-prime situations regularly work with people in exactly this position — recently separated, rebuilding, needing reliable transportation to get to work and manage a new life independently.

For borrowers in the 500-599 range (subprime) after a difficult separation, the key factors that lenders look at are:

- Stability of current income (even if recently started)

- Evidence the credit issues were circumstantial (separation-related) rather than habitual

- Reasonable debt-to-income ratio in your new single-income situation

- Some down payment if possible (even $1,000-$2,000 helps)

A reliable, affordable vehicle is often the foundation the rest of the post-separation rebuild is built on. Having a car payment you can make every month on time is one of the fastest ways to demonstrate to the credit bureaus — and future lenders — that the difficult period is behind you. Divorce car financing is a specialized area that our team understands deeply, and the Airdrie-based options are often more accessible than people expect.

Practical Vehicle Choices After Separation

When you're starting fresh financially, the vehicle you choose matters as much as the financing you get it on. A few considerations specific to post-separation buyers:

Prioritize reliability and low operating costs. You're now managing a budget solo. A vehicle with high fuel consumption, frequent repair needs, or expensive insurance will strain a newly single-income budget in ways that compound month over month. The Honda CR-V and Kia Sportage are popular choices for their balance of reliability, practicality, and reasonable operating costs across Alberta's seasons.

Right-size the vehicle to your actual life now. A family SUV that made sense for a two-parent household may be more vehicle than you need or can comfortably afford solo. A smaller crossover or sedan might serve your daily needs better and free up $100-$200/month that matters significantly as a single-income household.

Consider the full cost, not just the payment. Insurance, fuel, maintenance, and registration all need to fit your new budget. Use our payment calculator to model different vehicle price points and see how they fit your income.

Common Misconceptions About Joint Car Loans and Separation

A few beliefs come up repeatedly that are worth addressing directly, because acting on incorrect assumptions in this area causes real financial harm.

"The separation agreement handles it." A separation agreement is a binding contract between you and your former spouse — but it has no effect on the lender. The lender's contract is with both of you, and that contract doesn't change because your domestic situation changed. Courts can enforce separation agreements between the parties, but the lender can still pursue both of you for payment regardless of what the agreement says about who is "responsible."

"If I'm not driving the car, I'm not on the hook." Who drives a vehicle has no bearing on who is legally responsible for the loan. If your name is on the finance contract, you're responsible for the debt — period. Physical possession of the vehicle doesn't change financial liability.

"I can just sign over ownership." Transferring vehicle registration (the physical title/ownership document from Alberta Registries) and transferring financial liability on the loan are two completely separate processes. You can transfer the registration without touching the loan, which leaves one person with legal ownership of a vehicle but both people still on the hook for the debt. Both transfers need to happen for a true clean break.

"My credit won't be affected if I was never the primary borrower." On a joint car loan, there is no primary and secondary borrower in the way that term is sometimes used in marketing materials. Both co-applicants are equally liable and equally reported to the credit bureaus. Your credit score will be affected identically by payment history, regardless of whose income was used to qualify.

"The dealer can just take one name off." Dealerships facilitate financing, but they cannot unilaterally modify existing loan contracts. That requires the lender's involvement and typically a new credit application. If a dealership tells you they can simply remove a name from an existing loan without a new credit application, be skeptical — that's not how lenders work.

What to Expect When Refinancing During Separation

If you've decided to refinance the vehicle into one name, here's a realistic picture of the process so you're not caught off guard.

The refinancing lender will run a full credit application on the person assuming the loan. They'll look at credit score, employment income, debt-to-income ratio, and the vehicle's current value versus the outstanding loan balance. The key difference from an original purchase application is that the loan amount is set — it's the payoff amount on the existing loan — so the underwriting focuses almost entirely on whether the single applicant can support that obligation.

A common challenge is when separation has caused income disruption — one spouse left employment to care for children, for example, or recently changed jobs. If your income documentation is thin or your debt-to-income ratio looks strained as a single-income borrower, lenders who specialize in non-prime situations are often more flexible than traditional banks in evaluating the full context. They may ask for a letter of employment, recent pay stubs, bank statements showing consistent deposit patterns, and sometimes a co-signer if the numbers are tight.

The process of removing a co-signer from a car loan follows essentially the same path as a separation refinance — a new credit application, new approval, and new loan replacing the old one. The terminology is different but the mechanics are identical. Understanding that process gives you a clear picture of what to expect.

For borrowers who end up needing a fresh vehicle rather than refinancing an existing one, the application process through a multi-lender model gives you access to financing options across a range of lenders simultaneously — rather than applying one at a time and accumulating credit inquiries. Our Calgary-area divorce financing specialists can walk through your specific situation and identify which lenders are most likely to work with your current profile.

A Note on Timing

The instinct during separation is often to wait until everything is settled before making any financial moves. But waiting too long on the vehicle situation can create its own problems — credit damage from a disputed joint account can accumulate for months, and the longer the jointly held loan sits open, the more exposure both parties carry.

For the vehicle specifically, getting a clear plan in place early — even before lawyers have finalized everything — is usually better. Whether that plan is "we'll sell and split" or "I'll refinance in my name" or "we'll trade and each start fresh," having the plan agreed upon and moving toward execution protects both parties' credit and simplifies the rest of the proceedings.

Separation is hard enough without a car loan making it harder. If you're navigating a joint vehicle situation in Calgary or the surrounding area and need guidance on your options — financing to assume the loan, trading in the joint vehicle, or getting into your own vehicle for the first time — start with our financing application and we'll walk through what's realistic based on your current situation. There's no judgment here — just practical help getting to the other side with your finances intact.

Compare and Apply

- Complete Bad Credit Car Buying Guide (Alberta) — step-by-step guide to getting approved in Alberta

Financing Resources

Related Articles

Ready to Find Your Vehicle?

Browse our inventory or apply for financing. All credit situations welcome.

★★★★★ 89+ Google Reviews · AMVIC Licensed · Free Delivery 300km