What Is Negative Equity and How to Avoid Being Upside Down

In this article

- What Negative Equity Actually Means

- How Negative Equity Happens: The Timeline

- The Three Main Causes of Negative Equity

- 1. Long Loan Terms

- 2. No Down Payment (or a Small One)

- 3. Rapid Depreciation on Certain Vehicles

- How to Check if You're Upside Down Right Now

- Depreciation Rates by Vehicle Type: What Loses Value Fastest in Alberta

- The Private Sale Option: Getting Closer to Market Value

- Strategies to Avoid Negative Equity From the Start

- Put More Down

- Choose the Shortest Term You Can Afford

- Buy Vehicles That Hold Value

- Understand the Full Cost Before You Sign

- What to Do if You're Already Underwater

- Stay Put and Build Equity

- Make Extra Payments on the Principal

- Improve the Vehicle's Value

- Refinance to a Better Rate

- Negative Equity and Trade-Ins: The Critical Conversation

- Rolling Negative Equity Into a New Loan: Why It's Dangerous

- Negative Equity and Insurance Write-Offs

- The Bottom Line

- Related Buyer Guides

- Compare and Apply

Check Your Options in 3 Minutes

No credit impact. All credit situations welcome.

★★★★★ 89+ Google Reviews · AMVIC Licensed · Free Delivery 300km

Picture this: you bought a vehicle two years ago, life changed, and now you need to trade it in or sell it. You call the lender to get your payout figure — say, $28,500 — and then check what your vehicle is actually worth. The dealer offers $21,000. Your bank says maybe $23,000 private sale on a good day. That $5,000 to $7,500 gap between what you owe and what the vehicle is worth? That's negative equity on a car loan, and it's one of the most common financial traps Canadian vehicle owners fall into. Understanding how it works — and how to avoid it — can save you thousands.

See what you pre-qualify for

Three quick answers — soft check, no commitment.

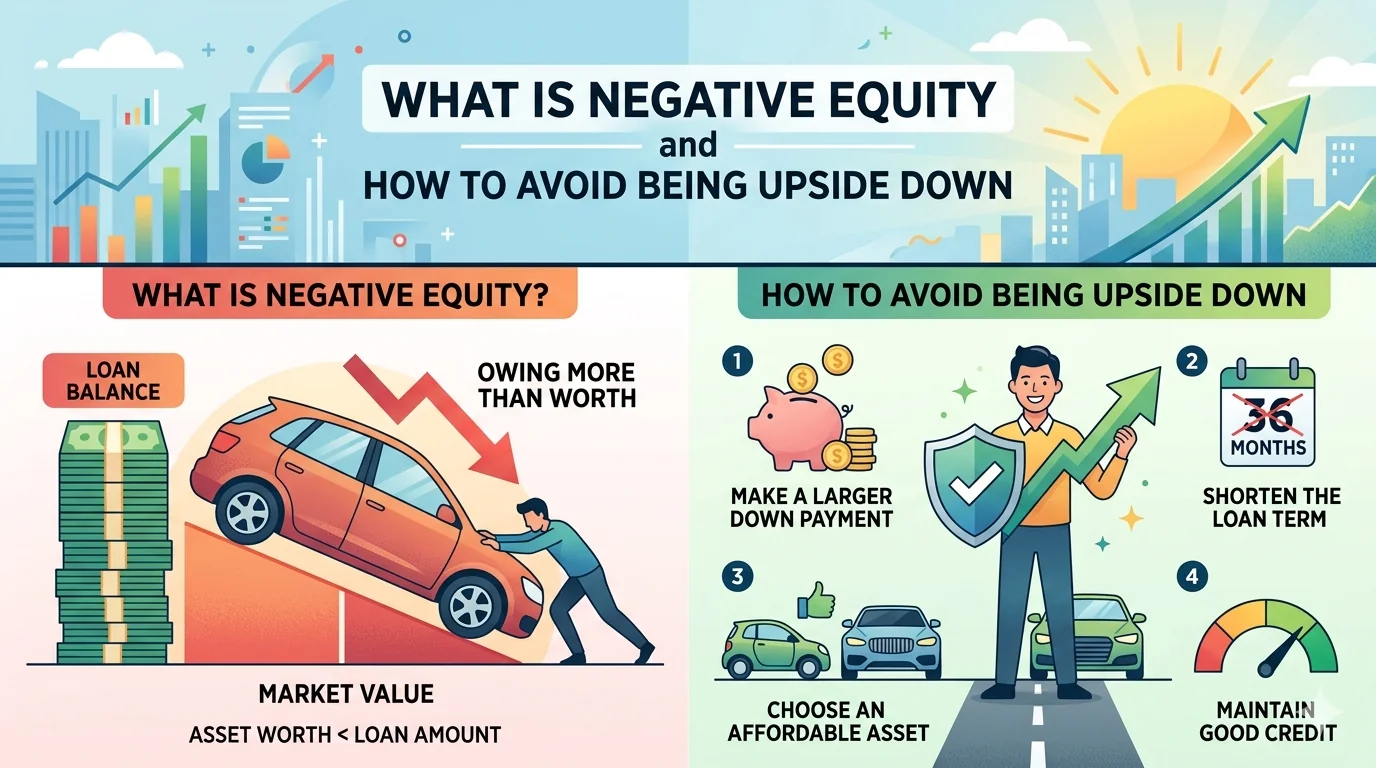

What Negative Equity Actually Means

Negative equity simply means your loan balance is higher than your vehicle's current market value. If you owe $30,000 on a truck that's worth $24,000, you're $6,000 upside down. You don't actually "own" anything in that vehicle — the lender owns it all, plus you'd still owe them $6,000 if you sold it today for full market value.

The term "upside down" is an apt description. In a healthy loan, equity flows in your direction: you owe less than the vehicle is worth, and the difference is yours. In negative equity, that relationship flips. You carry a liability, not an asset. And because vehicles are depreciating assets — they lose value every year no matter what you do — every vehicle loan starts with the potential for negative equity on day one.

Key point: A vehicle is not an investment. It's a depreciating asset. Structuring your loan poorly turns that inevitable depreciation into a trap.

How Negative Equity Happens: The Timeline

Negative equity doesn't happen because you made a bad decision. It happens because of how loan math interacts with vehicle depreciation — and most people are never shown that math before they sign.

Here's a realistic timeline for a typical used vehicle purchase in Alberta:

| Month | Loan Balance Remaining | Vehicle Market Value | Equity Position |

|---|---|---|---|

| Purchase (Month 0) | $26,000 | $26,000 | $0 (break-even) |

| Month 6 | $24,800 | $23,200 | -$1,600 |

| Month 12 | $23,600 | $21,000 | -$2,600 |

| Month 24 | $21,000 | $18,500 | -$2,500 |

| Month 36 | $18,200 | $17,200 | -$1,000 |

| Month 48 | $15,000 | $15,800 | +$800 (positive) |

| Month 60 | $11,500 | $14,000 | +$2,500 (positive) |

Notice how the loan balance stays stubbornly high in the early months — that's because early payments go mostly to interest, not principal. Meanwhile, the vehicle depreciates fastest in its first two years. The result is a window of negative equity that can last two to four years depending on your loan terms, rate, and down payment.

The deeper the negative equity hole and the longer the loan term, the longer that window stays open. On a 96-month loan with no down payment at a higher interest rate, you might be upside down for five or six years. Understanding how car loan amortization works makes this timeline much easier to visualize.

The Three Main Causes of Negative Equity

1. Long Loan Terms

The single biggest driver of negative equity is extending the loan term to reduce monthly payments. An 84-month or 96-month loan feels manageable — the payments are smaller, the vehicle seems affordable. But you're paying interest for seven or eight years on an asset that's worth a fraction of its original value by the time you're done. The loan balance shrinks far slower than the vehicle depreciates.

On a $25,000 vehicle financed at 14.99% with nothing down, here's what you'd owe vs. what the vehicle might be worth at the midpoint of the loan:

- 48-month loan: At month 24, owe ~$13,800 on a vehicle worth ~$17,500. Positive equity.

- 72-month loan: At month 36, owe ~$17,200 on a vehicle worth ~$16,000. Negative equity.

- 96-month loan: At month 48, owe ~$19,400 on a vehicle worth ~$14,500. Deep negative equity.

2. No Down Payment (or a Small One)

Walking into a purchase with zero down means you're starting the loan already at or past the break-even point, because the vehicle loses value the moment it leaves the lot. Even a modest 10% down payment ($2,600 on a $26,000 vehicle) gives you a cushion that keeps you out of negative equity for much longer.

In subprime financing, lenders often require a down payment precisely because they understand this math. A down payment reduces lender risk and gives you immediate positive equity. It's one of the few levers you can pull on day one. If you're weighing whether to put savings toward a vehicle purchase, the emergency fund vs. down payment decision deserves serious thought.

3. Rapid Depreciation on Certain Vehicles

Not all vehicles depreciate at the same rate. Luxury vehicles, certain domestic models, and vehicles with high cost-of-ownership reputations can lose 15-25% of their value in year one. If you finance one of these at full price with minimal down, you're underwater immediately and deeply.

By contrast, trucks like the Ford F-150 and vehicles like the Toyota RAV4 are historically strong value retainers in the Alberta market. High demand, low supply, and a reputation for durability keep their resale values elevated. Choosing a vehicle with strong resale is one of the most underrated tools for avoiding negative equity.

How to Check if You're Upside Down Right Now

If you're unsure where you stand, here's a four-step check you can do today:

- Get your loan payout amount. Call your lender or log into your account online. Ask for the "10-day payout figure" — this is what you'd need to pay the loan off in full right now.

- Get a realistic market value estimate. Check Canadian Black Book or AutoTrader.ca for comparable vehicles in your area (same year, make, model, trim, approximate kilometres). Be honest — use the average, not the optimistic high.

- Check a dealer's trade-in estimate. Bring the vehicle to a dealership and ask for a written trade-in appraisal without committing to buy anything. This is the most realistic number you'll get for what someone would actually pay for your vehicle today.

- Subtract payout from value. If the result is negative, you're upside down. If it's positive, you have equity.

Repeat this check every 12 months if you're in a longer-term loan. Knowing where you stand means you're never caught off guard when circumstances change.

Depreciation Rates by Vehicle Type: What Loses Value Fastest in Alberta

Not all vehicles depreciate at the same speed, and in Alberta's specific market — where truck demand is high, winters are severe, and outdoor recreation drives strong demand for capable SUVs — the depreciation curves look different than national averages suggest. Understanding this by vehicle category helps you make smarter purchase decisions from day one.

| Vehicle Category | Year 1 Depreciation (Approx.) | Year 3 Depreciation (Approx.) | Alberta Market Notes |

|---|---|---|---|

| Full-size trucks (F-150, Silverado, Ram) | 8-12% | 20-28% | Strongest retention in the province. Trades demand keeps prices high. |

| Japanese compact SUVs (RAV4, CR-V, Rogue) | 10-14% | 24-32% | Excellent retention. Short supply relative to demand keeps resale strong. |

| Domestic sedans (Impala, Fusion, Malibu) | 18-24% | 38-50% | Weak retention, especially as manufacturers discontinue models. |

| Luxury vehicles (BMW, Mercedes, Audi) | 20-30% | 45-55% | Steep drop after warranty expiry. High repair costs suppress demand for older units. |

| Electric vehicles | 15-30% | 40-55% | Highly variable. Range anxiety and charging infrastructure in rural Alberta compress resale. |

The takeaway: if you're financing with a modest down payment and a longer term, your negative equity exposure is dramatically lower in a truck or Japanese SUV than in a domestic sedan or luxury import. The vehicle choice is a financial decision, not just a preference decision — especially in the first three years of ownership.

There's also a seasonal component in Alberta. Truck and SUV values remain relatively stable through Alberta's long winters because buyers are always looking for capable vehicles. Convertibles and sports cars are harder to move in November in Calgary than in July in Vancouver. Buying a vehicle that matches Alberta's year-round demand profile isn't just practical — it supports your resale value when you eventually need to sell or trade.

The Private Sale Option: Getting Closer to Market Value

When you're carrying negative equity and want to exit the vehicle, there's one tool that can meaningfully reduce the gap: selling privately instead of trading in. A dealership trade-in appraisal is the lowest price the market will pay for your vehicle — dealers need room for reconditioning, markup, and profit. A private buyer, by contrast, pays closer to actual market value because they're eliminating the dealer's margin.

The difference between a dealer trade-in offer and a private sale is typically $1,500 to $4,000 depending on the vehicle. On a vehicle where you're $5,000 upside down, a private sale that nets $3,000 more than the trade appraisal suddenly means your gap is only $2,000 — a far more manageable shortfall to cover out of pocket before getting into your next vehicle.

The complication with private sales when you have an active loan: the lender holds the title (or a lien against the vehicle in Alberta's personal property registry), so you can't simply sign the title over to a private buyer at the kitchen table. You'll need to coordinate the payout with the lender and the buyer simultaneously — often using a lawyer or the buyer's financial institution to hold funds in trust during the transaction. It's more paperwork than a dealer trade, but for thousands of dollars in gap reduction, it's frequently worth it.

Strategies to Avoid Negative Equity From the Start

Put More Down

Every dollar you put down at purchase is a dollar of equity buffer on day one. Even if you can only manage 10-15% down, that cushion significantly shortens the period of negative equity. On a $22,000 vehicle, a $3,300 down payment (15%) means your starting loan is $18,700 — well below the vehicle's value before the first depreciation hit lands.

Choose the Shortest Term You Can Afford

The monthly payment difference between a 60-month and 84-month loan on $22,000 at 14.99% might be $120/biweekly. That feels significant. But you'll pay thousands more in total interest on the longer term, and you'll spend three extra years in negative equity. If a shorter term is at all possible — or becomes possible after you've saved a larger down payment — it's worth the sacrifice. Our payment calculator lets you compare what different terms actually cost you in total.

Buy Vehicles That Hold Value

In Alberta specifically, trucks, body-on-frame SUVs, and Japanese brands consistently hold their value better than most alternatives. The F-150, Toyota Tacoma, Toyota RAV4, and Honda CR-V are perennial value retention leaders. Alberta's mix of trades workers, rural owners, and outdoor enthusiasts keeps demand for capable vehicles strong year-round, which supports resale prices.

Understand the Full Cost Before You Sign

Get a complete breakdown of the total cost of the loan: total interest paid, total amount paid, amortization schedule for at least the first 24 months. If a lender or dealer is reluctant to show you this information, that's a signal. Transparency at the start is your best protection. Our team at Airdrie walks every customer through the full numbers before anything is signed — no surprises at delivery.

What to Do if You're Already Underwater

Already upside down? You're not alone, and you have options. None of them are painless, but some are significantly better than others.

Stay Put and Build Equity

If the vehicle is running well and you can afford the payments, the simplest move is often to keep making payments and let time do the work. Eventually — usually between month 30 and 48 depending on your loan — the balance and value lines will cross. You'll emerge with positive equity. Avoid the temptation to roll out of the vehicle early, because doing so just restarts the negative equity clock.

Make Extra Payments on the Principal

Adding extra money directly to the principal accelerates the timeline to positive equity. Even an extra $50 per biweekly payment on a $22,000 loan at 14.99% cuts months off your amortization and reduces the depth of negative equity in the early years. Confirm with your lender that extra payments apply to principal, not just advance the next payment date.

Improve the Vehicle's Value

Keeping the vehicle in top condition — addressing mechanical issues promptly, maintaining service records, protecting the exterior — preserves market value. A well-maintained vehicle with documentation sells for meaningfully more than the same vehicle with a spotty history. The guide on preserving trade-in value covers the specific steps that matter most to appraisers.

Refinance to a Better Rate

If your credit has improved since the original loan, refinancing to a lower rate reduces the interest you're paying and accelerates principal paydown. A drop from 19.99% to 14.99% on a $22,000 loan isn't just about monthly cash flow — it meaningfully changes how fast you build equity. Check what current car loan rates in Alberta look like for your credit tier before assuming your existing rate is the best you can do.

Negative Equity and Trade-Ins: The Critical Conversation

When you're upside down and want to trade in, the dealership will offer you a trade-in value for your vehicle. If that value is less than your payout, the difference — your negative equity — has to go somewhere. It usually goes into the new loan.

This is where many buyers make the situation significantly worse. Rolling $6,000 of negative equity into a new $28,000 loan means you're actually financing $34,000 — but a vehicle worth $28,000 is the collateral. You've just created deeper negative equity on day one of the new loan than you had on the old one.

Before trading in a vehicle with negative equity, get a written trade-in appraisal and compare it honestly to your payout. If the gap is manageable — $2,000 to $3,000 — and the new vehicle genuinely solves a problem (reliability, size, work requirements), the trade might still make financial sense. If the gap is $8,000 or more, you're digging a deeper hole. Consider holding the vehicle longer, paying down the balance faster, or selling privately to get closer to market value before trading.

Rolling Negative Equity Into a New Loan: Why It's Dangerous

This practice — often called "rolling equity" even when there is no equity — is one of the most common ways people get locked into a cycle of perpetual debt on depreciating vehicles. Here's the math in plain terms:

You owe $26,000 on a vehicle worth $20,000. That's $6,000 in negative equity. You trade in, and the dealer rolls that $6,000 into a new $32,000 vehicle purchase. Your new loan is $38,000 on a vehicle worth $32,000. You're already $6,000 underwater on a brand-new loan. Now add the normal first-year depreciation on the new vehicle — another $3,000 to $5,000 — and you're potentially $9,000 to $11,000 upside down six months after you thought you "started fresh."

GAP insurance can protect you from the worst outcome if the vehicle is written off or stolen. Understanding how GAP coverage works is essential if you do carry negative equity from one loan into another, because your regular insurance payout will only cover what the vehicle is worth — not what you owe.

The pattern to avoid: Negative equity → trade in early → new loan with rolled equity → more negative equity → trade in again. Each cycle compounds the problem. Break it by staying in the vehicle until you have positive equity.

Negative Equity and Insurance Write-Offs

Here's a scenario most people don't think about until it's too late: your vehicle is in an accident and written off. Your insurance pays out the "actual cash value" — what the vehicle was worth the moment before the accident. If you owe more than that, you're responsible for the difference out of pocket.

A $6,000 negative equity position combined with a total-loss accident means you owe the lender $6,000 with no vehicle to show for it. This is exactly what GAP insurance covers — the gap between the insurance payout and the outstanding loan balance. If you're carrying significant negative equity, GAP coverage isn't optional. Check what your current auto policy covers and whether your lender-provided GAP insurance is actually competitive.

The Bottom Line

Negative equity is not a character flaw — it's a math problem. Loan terms, down payment, interest rate, and vehicle selection all interact to determine how deep the negative equity window is and how long it lasts. Understanding those mechanics puts you in control. Choosing shorter terms, meaningful down payments, and vehicles with strong resale addresses the problem at the root.

If you're currently upside down or trying to structure a purchase to avoid it, our team works through the numbers with every customer. We look at negative equity financing options honestly — not to obscure the math, but to help you find the best path given where you actually stand. Start with our financing application or use the payment calculator to model different scenarios before you commit to anything.

Compare and Apply

- Bad Credit Financing — Complete Guide — Alberta's subprime auto financing guide

Financing Resources

Related Articles

Ready to Find Your Vehicle?

Browse our inventory or apply for financing. All credit situations welcome.

★★★★★ 89+ Google Reviews · AMVIC Licensed · Free Delivery 300km