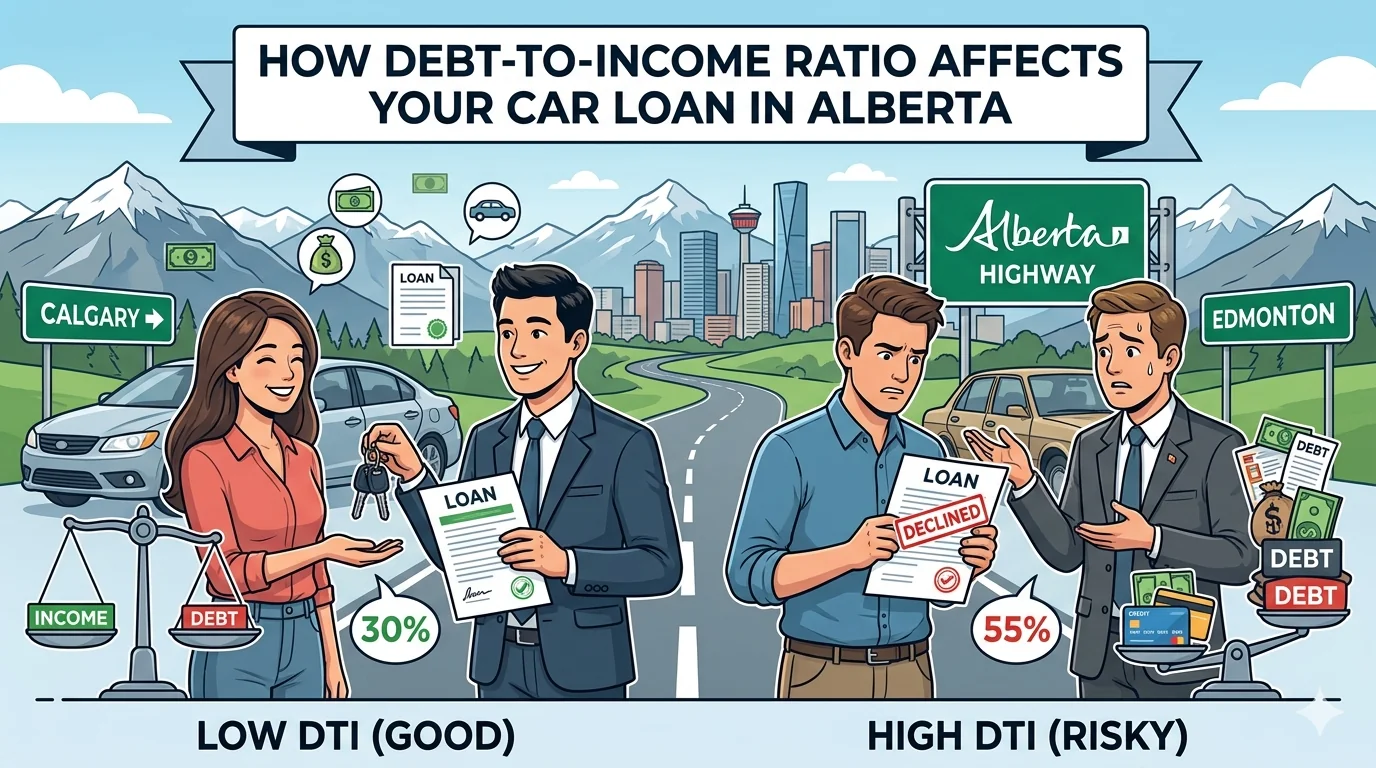

How Debt-to-Income Ratio Affects Your Car Loan in Alberta

In this article

- What Debt-to-Income Ratio Actually Means in Car Financing

- How to Calculate Your DTI Before You Apply

- What Alberta Lenders Consider Acceptable DTI

- How Existing Debts Eat Into Your Car Loan Capacity

- Mortgage or Rent

- Student Loans

- Credit Card Minimums

- Existing Car Payments

- Support and Alimony Payments

- Realistic DTI Scenarios at Alberta Income Levels

- Scenario 1: Airdrie Trades Worker, $7,500/Month Gross

- Scenario 2: Calgary Retail Worker, $3,400/Month Gross

- Scenario 3: Edmonton Professional, $9,000/Month Gross

- Strategies to Improve Your DTI Before Applying

- Pay Down Revolving Balances Before Applying

- Use a Tax Refund Strategically

- Increase Your Down Payment

- Choose a Longer Loan Term (Carefully)

- Add a Co-Applicant With Income

- Consolidate Higher-Minimum Debts

- DTI for Non-Traditional Income Situations

- The DTI-Credit Score Interaction

- What to Do If Your DTI Is Borderline

- How Alberta's Cost of Living Affects DTI Calculations

- DTI and the Timing of Your Application

- Making Your DTI Work for You

- Related Buyer Guides

- Compare and Apply

Check Your Options in 3 Minutes

No credit impact. All credit situations welcome.

★★★★★ 96+ Google Reviews · AMVIC Licensed · Free Delivery 300km

You've been making your payments on time. You have a steady job in Calgary. Your credit score sits in the 600s. And yet the lender came back saying you don't qualify for the loan amount you need. The culprit, more often than people expect, isn't your credit score at all — it's your debt-to-income ratio. This single metric, which most buyers have never calculated, quietly determines how much car you can actually afford to finance in Alberta.

See what you pre-qualify for

Three quick answers — soft check, no commitment.

What Debt-to-Income Ratio Actually Means in Car Financing

Debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward debt payments. Lenders use it to answer a simple question: after you make all your existing debt payments, plus the new car payment, how much financial cushion is left? A borrower carrying heavy existing debt is a different risk than an identical borrower with no obligations — even if their credit scores are the same.

There are two versions of DTI that matter in car financing:

- Total Debt Service (TDS): All monthly debt payments divided by gross monthly income. This includes your mortgage or rent, any existing car payments, credit card minimums, student loans, line of credit payments, and the proposed new car payment.

- Gross Debt Service (GDS): Housing costs only (mortgage principal + interest + property taxes + heat) divided by gross monthly income. Less relevant for car loans, but some lenders calculate it for context.

For car loan purposes, lenders are primarily focused on TDS. When you understand how car financing works in practice, DTI is one of the first filters an underwriter applies — before they get deep into your credit history.

How to Calculate Your DTI Before You Apply

The math is straightforward. Grab a recent pay stub or your last Notice of Assessment from CRA. Here's the formula:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

Let's walk through a realistic Alberta example. Sarah works in healthcare administration in Calgary. Her gross monthly income is $5,200. Here are her current monthly obligations:

| Obligation | Monthly Payment |

|---|---|

| Rent | $1,650 |

| Student loan | $280 |

| Credit card minimum (Visa $4,200 balance) | $126 |

| Personal line of credit | $95 |

| Current total | $2,151 |

Sarah's current DTI without any car payment: ($2,151 ÷ $5,200) × 100 = 41.4%. That's already at the upper limit of what most prime lenders will accept. If she adds a $450/month car payment, her TDS climbs to 49.9% — well above the threshold. That's why her application came back with a smaller-than-expected approval.

Use our affordability calculator to run your own numbers before sitting down with a lender. It factors in your income, existing obligations, and gives you a realistic payment range.

What Alberta Lenders Consider Acceptable DTI

There's no universal DTI threshold — it varies significantly by lender tier. This is one of the most important things to understand about the Alberta car financing landscape, because a ratio that disqualifies you at one institution may be perfectly acceptable at another.

| Lender Type | Typical Max TDS | Notes |

|---|---|---|

| Major banks (TD, RBC, BMO) | 40–42% | Strict. Little flexibility for borderline files. |

| Credit unions | 40–44% | More relationship-based. May flex slightly for members. |

| Near-prime lenders | 44–48% | Accept higher DTI with compensating factors (strong employment, large down payment). |

| Subprime lenders | 45–55%+ | Focus more on payment-to-income (PTI) than total DTI. Different program logic. |

The distinction between subprime and prime financing programs isn't just about credit score thresholds — it's also about which metrics underwriters prioritize. Subprime lenders often focus on payment-to-income (PTI), which is the car payment alone as a percentage of monthly income, rather than total debt service. A PTI of 15-20% is commonly the subprime benchmark, meaning a buyer earning $4,500/month gross might qualify for a car payment up to $675-$900, even if their total DTI looks high by prime standards.

How Existing Debts Eat Into Your Car Loan Capacity

Every monthly obligation on your credit bureau is a line item eating into your available borrowing room. Here's how the most common Alberta debt types affect your car loan capacity:

Mortgage or Rent

This is usually the largest number in the DTI calculation, and it's often non-negotiable in the short term. A Calgary renter paying $1,800/month for a two-bedroom is starting from a significantly different position than an Airdrie homeowner with a $1,400 mortgage payment — even at the same income level. Lenders use the actual payment showing on your file or your stated rent, verified against bank statements.

Student Loans

Student loans are a significant factor for younger Alberta buyers in their late 20s and 30s. If your National Student Loan is $340/month and a provincial loan adds another $180/month, that's $520 monthly before you've spent a dollar on a car. Some lenders will exclude student loans in repayment hold or deferment status from the DTI calculation, but only if you can document the deferral in writing.

Credit Card Minimums

Lenders use the minimum payment showing on your credit bureau, not what you actually pay. A Mastercard with a $6,000 balance shows a minimum of approximately $180/month on bureau — even if you pay $500/month. High revolving balances with large minimums can significantly compress your DTI, which is one reason budgeting carefully before a car purchase includes paying down revolving debt, not just saving for a down payment.

Existing Car Payments

If you're already making a car payment on a vehicle you plan to trade in, that payment is still on your bureau until the trade-in pays it out. During the period between application and deal completion, lenders count it as an active obligation. This is why trading in a vehicle with an existing loan can be more complex than trading in something you own outright.

Support and Alimony Payments

Court-ordered support payments count as monthly obligations in the DTI calculation, even though they don't show on your credit bureau. Lenders ask about them on the application, and bank statements during verification typically reveal them. Accurate disclosure upfront is always the right call.

DTI reality check: A buyer earning $6,000/month gross with $2,000 in existing obligations can comfortably support a car payment around $400-$480/month at prime lender thresholds. Stretch above that, and you need a subprime lender or a restructured deal.

Realistic DTI Scenarios at Alberta Income Levels

Let's run three realistic Alberta profiles through the DTI math to see how different situations play out:

Scenario 1: Airdrie Trades Worker, $7,500/Month Gross

Mike is a journeyman electrician in Airdrie earning $7,500/month. His obligations: $1,950 mortgage, $320 truck payment (current vehicle he's keeping), $210 credit card minimums. Total obligations: $2,480. Current DTI: 33.1%. He can comfortably add a $600-$700 car payment and stay under prime lender thresholds. He has the room to finance a quality used Toyota Highlander or similar family SUV without stressing his DTI.

Scenario 2: Calgary Retail Worker, $3,400/Month Gross

Jen works full-time retail in Calgary at $3,400/month gross. Her obligations: $1,350 rent, $180 student loan, $95 credit card minimum. Total: $1,625. Current DTI: 47.8%. She's already above prime thresholds before any car payment. Even a modest $350/month payment pushes her to 58.1%. This is a file where subprime lenders with PTI-focused programs are the realistic path, and maximizing the down payment reduces the required loan amount — and therefore the monthly payment. Our page on down payment strategies for challenging credit situations applies directly here.

Scenario 3: Edmonton Professional, $9,000/Month Gross

David is a senior project manager at a pipeline company earning $9,000/month gross. His obligations: $2,850 mortgage, $430 line of credit, $220 credit card minimums. Total: $3,500. Current DTI: 38.9%. He has room for up to $650/month in car payment while staying under 46%. He's a prime candidate, and lenders will compete for his file. He could finance a late-model truck or a used Honda CR-V at competitive rates with multiple approval options.

Strategies to Improve Your DTI Before Applying

If your DTI is too high for the vehicle you need, you're not stuck. There are concrete steps that move the needle — some quickly, some over a longer horizon.

Pay Down Revolving Balances Before Applying

Credit card balances affect DTI through their minimum payments. Paying a $5,000 card balance down to $1,500 reduces the minimum from roughly $150/month to $45/month — freeing up $105/month in DTI capacity. That $105 could support an additional $3,000-$4,000 in loan capacity at typical rates. This is one of the highest-leverage moves before a car loan application.

Use a Tax Refund Strategically

Alberta's tax season typically produces refunds for W2-equivalent earners in spring. Using that refund to eliminate a specific debt rather than spreading it thin can have an outsized DTI impact. Eliminating a $180/month student loan payment entirely beats paying $180 toward eight different balances.

Increase Your Down Payment

A larger down payment reduces the loan amount, which reduces the required monthly payment. If you need a $350/month payment to fit your DTI but the vehicle would normally require $500/month at full financing, a down payment that bridges that gap is a direct solution. Our payment calculator lets you adjust down payment amounts to see how they shift monthly payments.

Choose a Longer Loan Term (Carefully)

Extending from a 60-month term to an 84-month term on an $18,000 loan at 12.99% drops the biweekly payment from roughly $222 to $170 — a real DTI improvement. The trade-off is more total interest paid over the life of the loan. For a buyer with limited DTI headroom, the longer term may be the only path to approval — but it's worth understanding the full cost. Financing terms from 12-96 months are available, and the right choice depends on your complete financial picture, not just monthly payment size.

Add a Co-Applicant With Income

Adding a spouse or partner with verifiable income to the application combines both incomes in the DTI denominator. If your partner earns $4,000/month and yours is $3,500/month, the combined $7,500 gross income makes the same set of obligations look dramatically different in DTI terms. This is different from a cosigner (who guarantees the loan but doesn't necessarily add income to the DTI calculation).

Consolidate Higher-Minimum Debts

If you're carrying multiple high-minimum debts, consolidating them into a single lower-rate installment loan can reduce the total monthly payment showing on bureau. Our debt consolidation calculator can help you model whether consolidation makes financial sense in your situation before you take that step.

DTI for Non-Traditional Income Situations

DTI calculation gets more complicated when your income isn't a predictable monthly salary. Alberta has a large proportion of self-employed workers, oilfield contractors, seasonal workers, and gig workers — all of whom face more scrutiny on the income side of the DTI equation.

For self-employed applicants, lenders typically use line 15000 (total income) from your NOA, not your business's gross revenue. After business deductions, the income lenders use is often significantly lower than what you actually take home — even though tax deductions are mathematically rational for you as a business owner. Some lenders have programs that accept bank statement income (deposits over 12-24 months) rather than NOA income, which better reflects cash flow for self-employed buyers.

Seasonal workers face similar challenges. An oilfield worker who earns $120,000 in eight months of active work shows seasonal income gaps on bank statements. Lenders annualize the income if it's consistent year-over-year (documented by two years of NOAs), but a single year with a gap can create friction. Knowing which lender programs accommodate your specific income pattern before applying is where working with a multi-lender broker pays off.

The DTI-Credit Score Interaction

DTI and credit score work together — not independently. A high credit score can sometimes compensate for a stretched DTI. A prime borrower with a 730 beacon score and a 46% TDS may still get approved where a subprime borrower with a 570 score and the same DTI would not, because the higher score signals lower probability of default. Similarly, a very low DTI can sometimes compensate for a lower credit score, because the financial headroom reduces the lender's risk even if the credit history is imperfect.

This interaction is why blanket advice ("you need a credit score above X to get a car loan") misses the point. The combination of DTI, credit score, down payment, vehicle value, and income stability is what underwriters are actually evaluating. Our page on serving the Calgary area includes more context on local lender availability and how we match buyers to the right program.

What to Do If Your DTI Is Borderline

If your DTI calculation lands in the 42-50% range after adding a car payment — the grey zone between prime and subprime thresholds — you're not automatically out of options. Here's the decision tree:

- Calculate your PTI independently. If the car payment alone is 15-18% of gross monthly income, subprime programs may still approve you even with a high total DTI.

- Identify which existing obligation you can most easily reduce or eliminate before applying. Even a 30-day delay to pay off a small loan can shift your DTI from borderline to acceptable.

- Determine your realistic down payment maximum. More down means less loan means lower payment means better DTI math.

- Consider the vehicle price range. A used Kia Forte at $14,000 produces a meaningfully lower payment than an $18,000 crossover — and may fit your DTI where the more expensive vehicle doesn't.

- Work with a multi-lender broker who can identify which specific lender programs fit your DTI profile without burning hard inquiries across institutions trying yourself.

How Alberta's Cost of Living Affects DTI Calculations

Alberta's higher-than-average cost of living — particularly in Calgary and Edmonton — means buyers here often carry higher rent and mortgage obligations than the national average. The Canada Mortgage and Housing Corporation data consistently shows Calgary rental costs among the highest in western Canada. A buyer in Lethbridge or Red Deer with identical income and credit to a Calgary renter will often have meaningfully more DTI room for a car payment, simply because housing costs less.

This geographic reality matters when you're comparing yourself to national approval statistics or rule-of-thumb DTI benchmarks written with Ontario or BC housing markets in mind. A 44% TDS that's perfectly acceptable for a Windsor homeowner paying $1,100/month in mortgage costs may look completely different for a Calgary renter paying $1,900/month for a comparable apartment. Alberta-specific income context — oil and gas wages, trades premiums, agricultural income — also means income levels here skew higher, which partially offsets the housing cost pressure for many buyers.

The practical implication: calculate your DTI using your actual Alberta numbers, not national averages. What matters is your specific ratio, not where you fall relative to a national benchmark that doesn't reflect your cost of living.

DTI and the Timing of Your Application

One often-overlooked factor is timing. Your DTI is a snapshot — it changes every time a debt is paid off, every time a balance changes, and every time your income changes. Applying in March after you've received a tax refund and used it to eliminate a loan is a structurally better position than applying in December when holiday credit card balances are at their peak.

Alberta's energy sector creates meaningful income timing for workers on project-based or seasonal schedules. Applying for a car loan mid-project when paycheques are flowing produces a very different bank statement picture than applying during a gap between contracts. If you have control over the timing of your application — and many buyers do — choosing a window when your income documentation is strongest and your balances are lowest is a simple, no-cost way to improve your DTI optics before a lender sees your file.

Making Your DTI Work for You

Debt-to-income ratio is one of those concepts that sounds technical but boils down to a simple reality: lenders want to see that a new car payment fits comfortably within your monthly cash flow. The math is yours to calculate before you ever walk into a dealership — and knowing your DTI in advance puts you in a much stronger position to choose the right vehicle at the right price point.

If you're managing a higher DTI and aren't sure which path makes the most sense for your situation, the best first step is an honest look at your complete financial picture. Our team has helped buyers across a wide range of DTI profiles find financing that actually works — not just on paper, but in their monthly budget.

Ready to see where your DTI lands and what it means for your options? Start your financing application and we'll work through it with you — no pressure, no obligation, just a clear picture of what's available.

Compare and Apply

- Complete Bad Credit Car Buying Guide (Alberta) — how to buy a car with bad credit in Alberta

Financing Resources

Related Articles

Ready to Find Your Vehicle?

Browse our inventory or apply for financing. All credit situations welcome.

★★★★★ 96+ Google Reviews · AMVIC Licensed · Free Delivery 300km